Many foreign professionals in Germany know the feeling.

You have a good job.

You earn a solid salary.

You work hard.

You pay your bills on time.

And still, at the end of the month, you ask yourself:

“I earn quite well — so why am I not really building wealth?”

Let us take a simple example.

Alex is 30 years old. He is single, lives alone in Germany, and works as an employed IT engineer. His tax class is Steuerklasse 1, the usual tax class for single employees.

His salary sounds impressive:

€6,000 gross per month

That means €72,000 gross per year.

For many people, this sounds like a very comfortable income.

But in Germany, one important rule applies:

Gross salary is not the money you actually receive.

Every month, Alex pays around €1,074 in wage tax, called Lohnsteuer. He also pays social security contributions for pension insurance, health insurance, unemployment insurance and long-term care insurance.

Assuming statutory health insurance and no church tax, his monthly deductions may look roughly like this:

Pension insurance: approx. €558

Health insurance: approx. €508

Unemployment insurance: approx. €78

Long-term care insurance: approx. €139

At the end, his monthly net salary is approximately:

€3,640

That is not a bad income.

But anyone living in Germany knows how quickly money disappears.

Rent, insurance, groceries, transport, phone bills, travel, family visits abroad, emergencies and maybe one or two holidays a year — suddenly the good salary feels much smaller.

Alex saves money every month.

He is disciplined.

He has no consumer debt.

He has a stable job.

His employer is happy with him.

But one evening he asks himself:

“Do I only want to work for money — or can I make my salary work for me?”

A friend who understands real estate shows him an apartment in Berlin.

The apartment has 89 m², 4 rooms, and the purchase price is €379,000.

It is already rented out. An older couple lives there and pays rent reliably every month.

The rent is:

Cold rent: €700

Warm rent: €870

Alex looks at the purchase price and says:

“€379,000? I do not have that kind of money.”

His friend smiles.

“You do not need to have the full amount. That is what bank financing is for.”

Alex considers buying the apartment with 90% financing.

The bank loan would be:

€341,100

The interest rate is assumed to be 4% per year.

The repayment of principal is assumed to be 2% per year.

Together, this creates an annual loan burden of 6%.

That means Alex has to pay the bank approximately:

€1,705.50 per month

Now Alex becomes quiet.

The tenant pays €870 warm rent every month. But as the owner, Alex has to pay monthly Hausgeld to the building management.

In this example, the Hausgeld is €340 per month.

A very simplified cash calculation looks like this:

€870 warm rent

minus €340 Hausgeld

= €530 remaining monthly rental cash flow

The bank payment is €1,705.50.

So at first glance, the calculation looks painful:

€1,705.50 bank payment

minus €530 remaining rent

= approx. €1,175.50 monthly burden

Alex says:

“Wait a second. I am supposed to pay almost €1,200 every month from my own salary? Why would I do that?”

That is the question most employees ask.

And it is a good question.

But this is where the investor’s view begins.

The bank payment is not one single type of cost. It consists of two different parts:

Interest and repayment of principal.

Interest is the cost of borrowing money.

But repayment of principal is different. It does not simply disappear. It reduces the loan and increases Alex’s equity in the property.

In other words:

Part of his monthly payment is not consumption. It is wealth building.

Now comes the tax side.

Because the apartment is rented out, the interest on the loan can generally be treated as a rental-related expense.

With a loan of €341,100 and an interest rate of 4%, Alex pays:

€13,644 interest per year

This interest is important because it reduces the taxable result from the rental property.

But interest is not the only important tax item.

There is another one many foreign employees in Germany do not know:

AfA — Absetzung für Abnutzung

In English, this means depreciation.

For many existing residential buildings, the standard depreciation is 2% per year on the building portion. However, the exact depreciation rate depends on the building type and completion date.

It is also important that depreciation does not apply to the land portion. It applies only to the building portion.

Let us use a simple assumption.

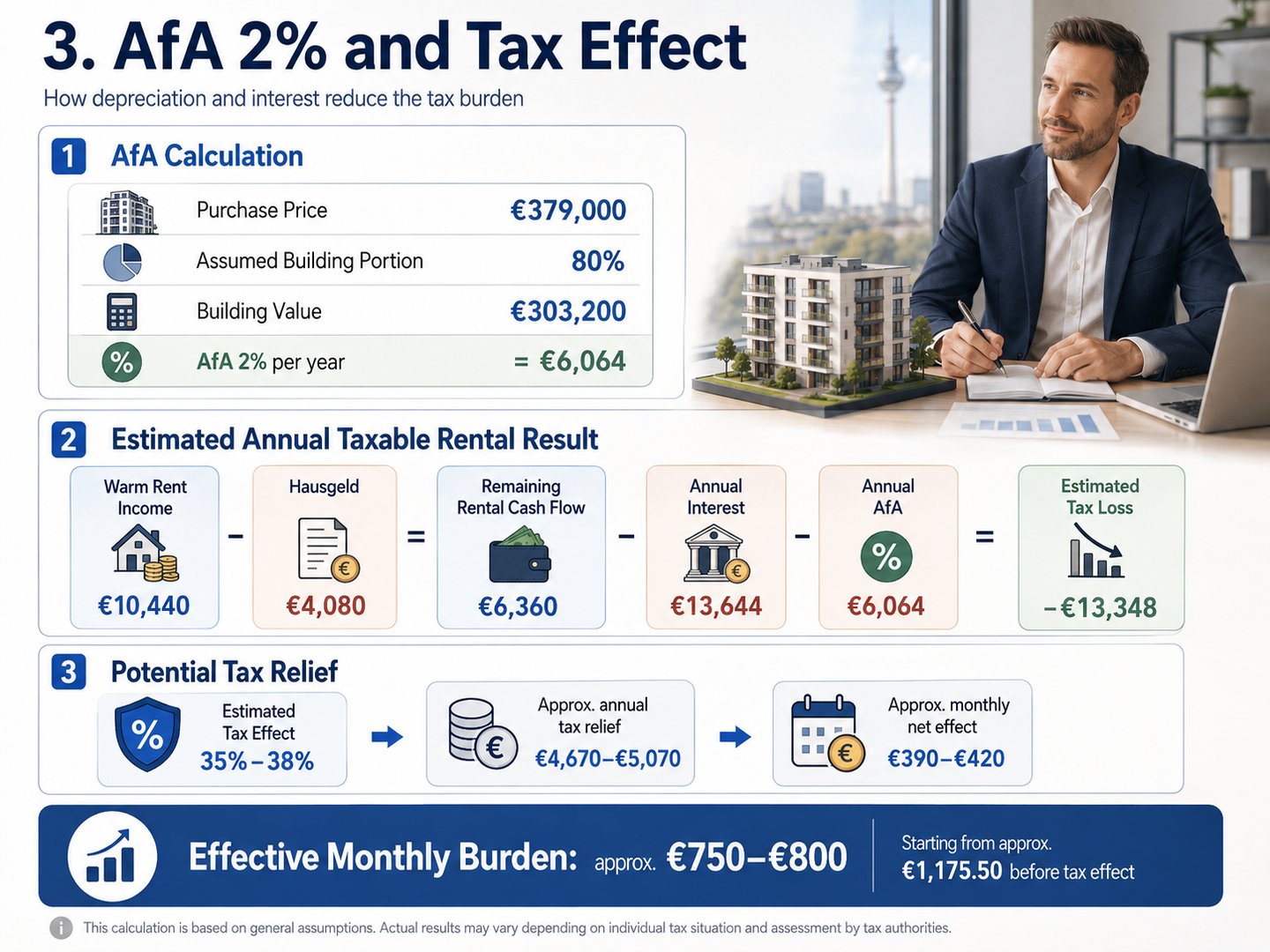

Purchase price: €379,000

Assumed building portion: 80%

Building value: €303,200

Now apply 2% AfA:

€303,200 × 2% = €6,064 per year

That is around:

€505 per month

But here is the interesting part:

Alex does not actually pay this €505 every month to anyone.

It is not a bank payment.

It is not a repair invoice.

It is not a cash expense.

But for tax purposes, it can reduce his taxable rental result.

That is why AfA is powerful.

It is a non-cash tax expense.

Now let us look at the simplified annual rental calculation:

Warm rent income:

€870 × 12 = €10,440

Hausgeld:

€340 × 12 = €4,080

Remaining rental cash flow before financing:

€6,360

Now deduct interest:

Annual interest:

€13,644

And deduct AfA:

Annual AfA:

approx. €6,064

Simplified tax result:

€6,360

minus €13,644 interest

minus €6,064 AfA

= approx. -€13,348

That means the rental property may create a tax loss of around:

€13,348 per year

Of course, the real calculation must be done more carefully.

Not every part of the Hausgeld is treated the same way. Some costs may be passed on to the tenant, others may not. The maintenance reserve, property management costs, repairs, purchase costs, notary fees and the building/land split must be reviewed individually.

But for a blog example, the main point is clear:

Interest plus AfA can create a tax loss from rental property.

And this tax loss can reduce the employee’s overall income tax burden.

Usually, employees wait until the following year, file a tax return, and then receive a refund.

In Germany, however, there is also the possibility to apply for a Lohnsteuer-Ermäßigung, a wage tax reduction.

In simple words:

Alex can ask the tax office to consider expected deductible expenses or losses already during the year.

If accepted, his monthly wage tax can go down.

That means his monthly net salary can go up.

However, there is an important limitation:

For rental losses from a newly acquired building, the allowance is generally only possible from the calendar year following the year of acquisition or completion. Therefore, the timing must be checked carefully.

Also, this is not a gift from the government.

It is more like the tax office saying:

“If you expect deductible losses, we may allow them to reduce your monthly wage tax during the year instead of waiting until the annual tax return.”

In Alex’s case, his annual wage tax is around:

€12,891.96

If the rental property creates an estimated tax loss of around €13,348, and if the tax effect is roughly 35% to 38%, the possible tax relief may be around:

€13,348 × 35% = approx. €4,670 per year

€13,348 × 38% = approx. €5,070 per year

That means a monthly effect of around:

€390 to €420 more net salary per month

With additional deductible costs, the effect may be somewhat higher. But it would not be responsible to promise a fixed amount.

The real result depends on income, exact expenses, financing terms, the building/land split, the tax office’s assessment and the final annual tax return.

Now Alex looks again at the monthly burden.

Before tax effect:

Bank payment: €1,705.50

Remaining rent after Hausgeld: €530

Monthly burden: approx. €1,175.50

After estimated tax effect:

€1,175.50

minus approx. €400 tax relief

= approx. €775 effective monthly burden

So the apartment that first looked like a monthly loss of almost €1,200 may feel more like a real burden of around:

€750 to €800 per month

This changes the perspective.

At first, Alex thought:

“I am losing €1,200 every month.”

But after understanding the structure, he sees something different.

The tenant pays part of the financing.

The bank provides the capital.

The tax system recognizes interest and depreciation.

Alex contributes part of his salary.

And over time, this contribution helps him build real estate assets.

This is the difference between spending money and building wealth.

Of course, buying real estate is not risk-free.

Repairs can occur.

Hausgeld can increase.

Interest rates can change.

Tenants can cause problems.

Regulations can change.

Property prices may not rise as expected.

Also, 90% financing does not mean that Alex needs no equity at all.

He usually still needs money for the remaining purchase price, real estate transfer tax, notary costs, land register costs and, in many cases, broker fees.

That is why nobody should buy just any apartment.

The location, purchase price, rental situation, building condition, Hausgeld, maintenance reserve, owners’ association documents, financing terms and tax effect must all be checked carefully.

But if the numbers make sense, a rented apartment can become a powerful wealth-building tool for an employed foreign professional in Germany.

There is another long-term point.

If a privately held rented property is sold after more than ten years, a private sale may generally fall outside the German taxation of private real estate sales.

Nobody knows what a Berlin apartment will be worth in ten years.

It may rise strongly.

It may rise moderately.

It may not rise much at all.

But if the property increases in value and the legal conditions are met, the capital gain may be tax-free after the ten-year period.

That is one reason why real estate can be attractive in Germany.

The real message is not:

“Buy any apartment and you will become rich.”

That would be dangerous and unrealistic.

The real message is:

If you are an employed foreign professional in Germany, your salary should not only pay your rent, insurance and living costs. It can also become the foundation for long-term asset building.

A single employee in Germany has several possible paths to build wealth.

First, they can buy a rented investment property and use bank financing, rental income, deductible interest, AfA and tax planning to build long-term assets.

Second, if their personal life develops in that direction, marriage can change household tax planning. Of course, nobody should marry for tax reasons. But in Germany, married couples may have different tax class options, and those options can influence monthly household cash flow.

Third, they can combine family planning and real estate investment. Two incomes, shared expenses and long-term planning can create a stronger financial base.

Fourth, they can think about both an investment property and a self-used home. One property may be rented out, while another may be used as their own residence. Owner-occupied property has its own tax rules and may under certain conditions be sold tax-free even before ten years.

The important point is simple:

A high salary alone does not automatically create wealth.

What matters is what you do with the salary.

Does it disappear into consumption?

Does it stay in a savings account?

Or does it help you buy assets?

Alex is still an IT engineer.

He still goes to work.

He still attends meetings.

He still pays taxes.

He still pays social security contributions.

But after buying the apartment, something changes.

Part of his salary no longer disappears into daily life.

Part of his salary becomes property.

The tenant helps through rent.

The bank helps through financing.

The tax system helps by recognizing costs.

And Alex helps himself through discipline and long-term planning.

That is the moment when salary income becomes more than monthly survival.

It becomes a structure for building assets.

Not overnight.

Not without risk.

Not without careful calculation.

But for many foreign professionals in Germany, it can be a realistic way to start building wealth.

The question is therefore not only:

“How much do I earn?”

The better question is:

“What does my salary create for me?”

Short disclaimer

This example is simplified and for educational purposes only. Real tax results depend on personal income, financing terms, the building/land split, deductible costs, rental contract, property condition, purchase costs, tax office assessment and the final annual tax return. Before buying property, foreign employees in Germany should consult a tax advisor, financing specialist and real estate professional.

Free Consultation

Have questions about entering the German market? Request a free consultation.

Request Free Consultation