For international buyers, the main challenge is usually not whether they are legally allowed to buy property in Germany. Foreign buyers can generally purchase real estate in Germany. The more important question is whether a bank is willing to finance the purchase, and under what conditions.

Residence status, employment situation, income, equity, credit history and the property itself all play an important role. Buyers who do not yet have permanent residence in Germany may still be able to obtain mortgage financing, but the case is usually reviewed more carefully.

What banks usually look at

German banks are generally conservative lenders. They want to understand whether the buyer can afford the monthly payments not only today, but also over the long term.

A temporary residence permit does not automatically prevent financing. However, it can make the process stricter. Fewer banks may be willing to finance the purchase, and the buyer may need more equity.

For a cautious but realistic calculation, a 70% financing scenario can be useful. With strong income, stable employment and sufficient savings, 80% financing may also be possible in suitable cases.

The important point is that many banks expect the purchase costs — real estate transfer tax, notary fees, land register fees and broker fees — to be paid from the buyer’s own funds, especially where the buyer has a temporary residence permit or only a short German credit history.

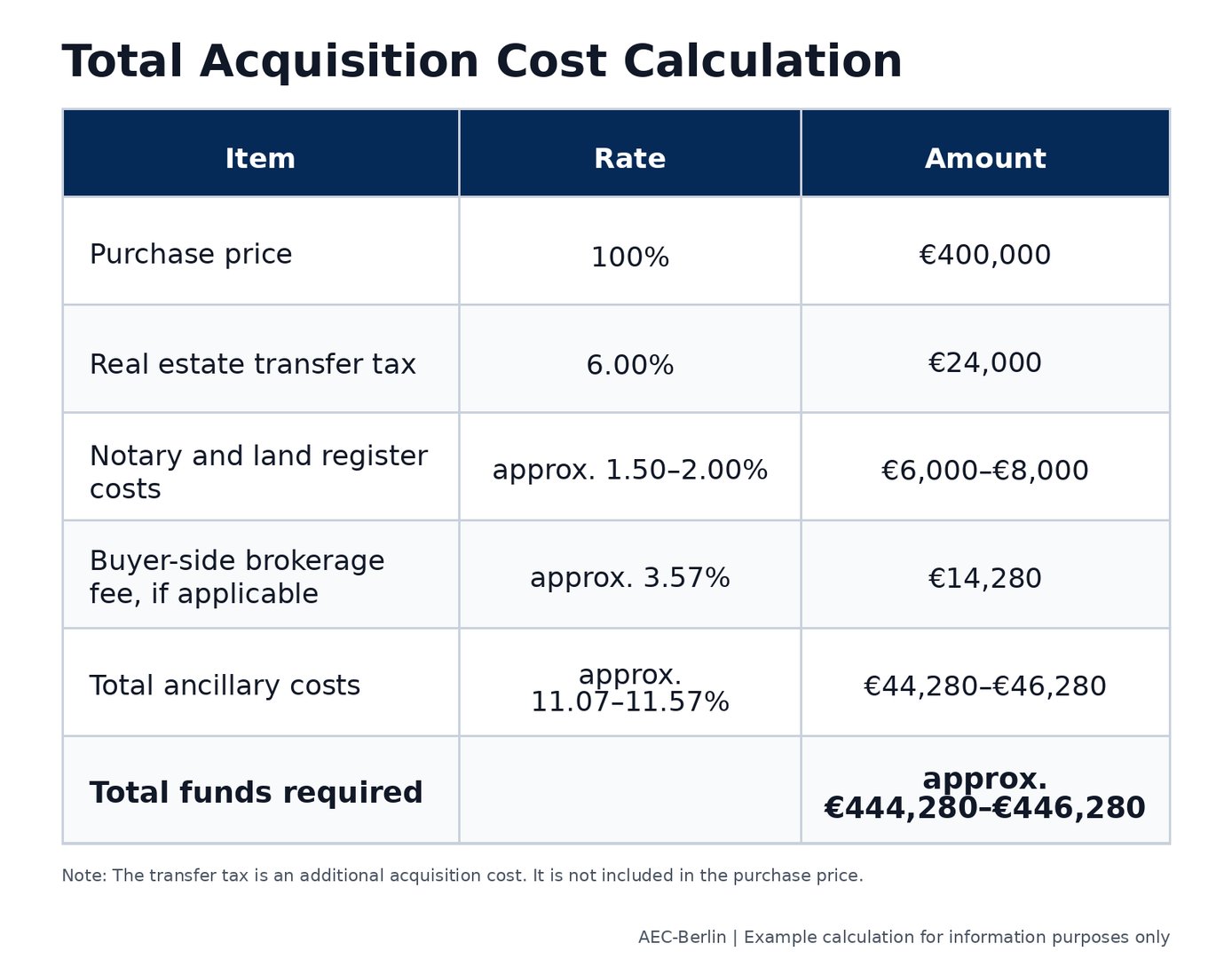

Example: buying an apartment in Berlin for €400,000

Let us use a simple example: an apartment in Berlin with a purchase price of €400,000.

In Berlin, the real estate transfer tax is currently 6% of the taxable consideration. In a standard property purchase, the taxable consideration is mainly the purchase price. In special cases, it can also include certain obligations assumed by the buyer or rights reserved by the seller.

The real estate transfer tax is not included in the purchase price. It is an additional acquisition cost payable after the notarised purchase agreement. In practice, the purchase contract usually states that the buyer must pay the tax.

For a €400,000 apartment in Berlin, the real estate transfer tax is therefore €24,000.

In addition, the buyer should calculate notary and land register costs, typically estimated at around 1.5–2.0% in practical purchase calculations.

In Berlin, apartments are often sold through real estate agents, so the buyer’s brokerage fee should also be included where applicable. For residential apartments and single-family homes, German law limits how broker fees can be passed on to the buyer. If the broker acts for both parties, the buyer cannot be charged more than the seller. If only one party has instructed the broker and later passes on part of the cost, the buyer’s share is also limited by law.

In many practical Berlin purchase calculations, a buyer-side broker fee of around 3.57% including VAT is used where a broker is involved.

This means that a €400,000 apartment does not only require €400,000. In a brokered transaction in Berlin, realistic total acquisition costs including typical buyer-side ancillary costs may be around €444,000–€446,000. Without a broker, the total amount would be lower.

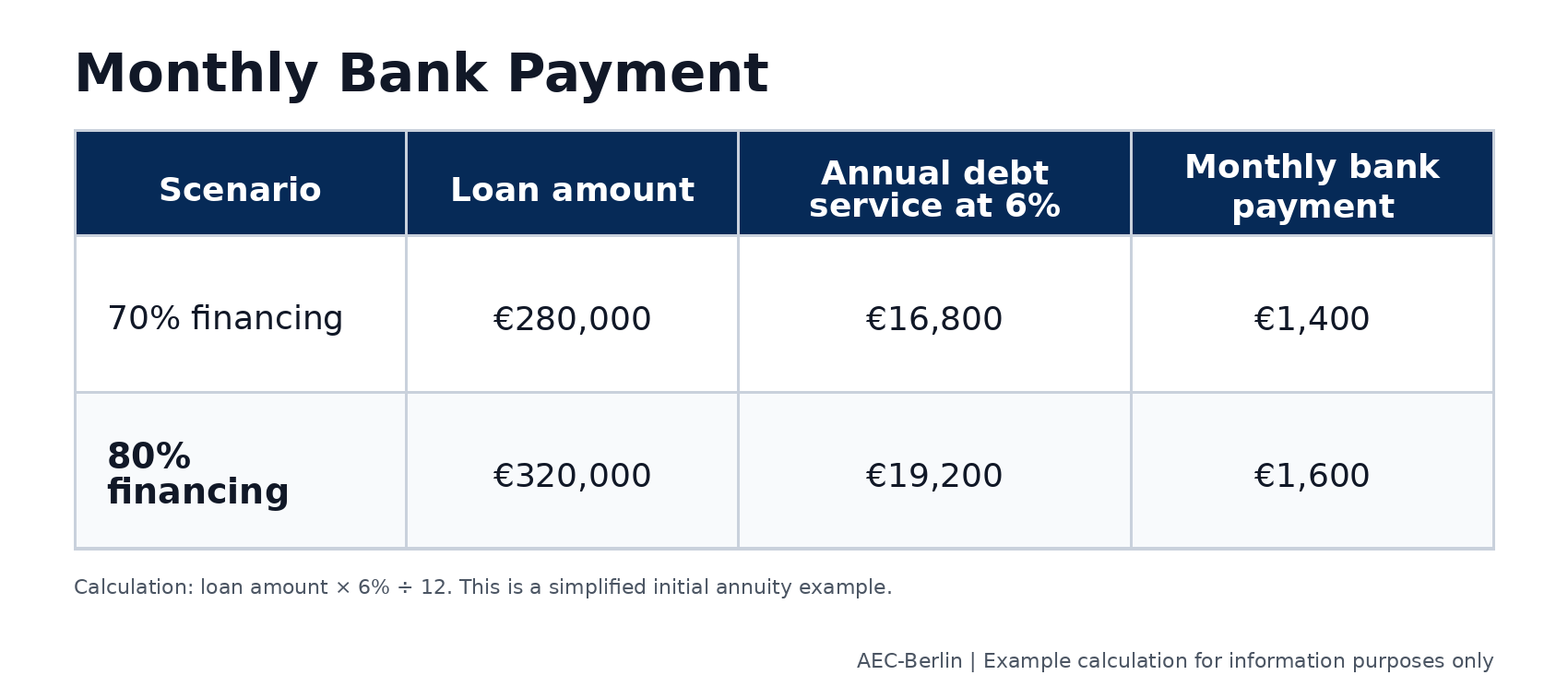

Financing scenarios: 70% and 80%

For international buyers with stable employment but no permanent residence yet, it is often too pessimistic to assume that only 50% financing is possible. A more practical approach is to calculate with 70% financing as a cautious case and 80% financing as a stronger-case scenario.

In this example, 70% financing means a loan of €280,000. The buyer would need to cover the remaining purchase price of €120,000 plus the acquisition costs from their own funds. With total acquisition costs of approximately €44,280–€46,280, the total equity requirement would be approximately €164,280–€166,280.

With 80% financing, the loan amount would be €320,000. The buyer would need to cover the remaining purchase price of €80,000 plus the acquisition costs. The total equity requirement would therefore be approximately €124,280–€126,280.

These figures are simplified examples. The final financing structure depends on the buyer’s income, employment situation, residence status, credit profile, the property value and the bank’s internal lending policy.

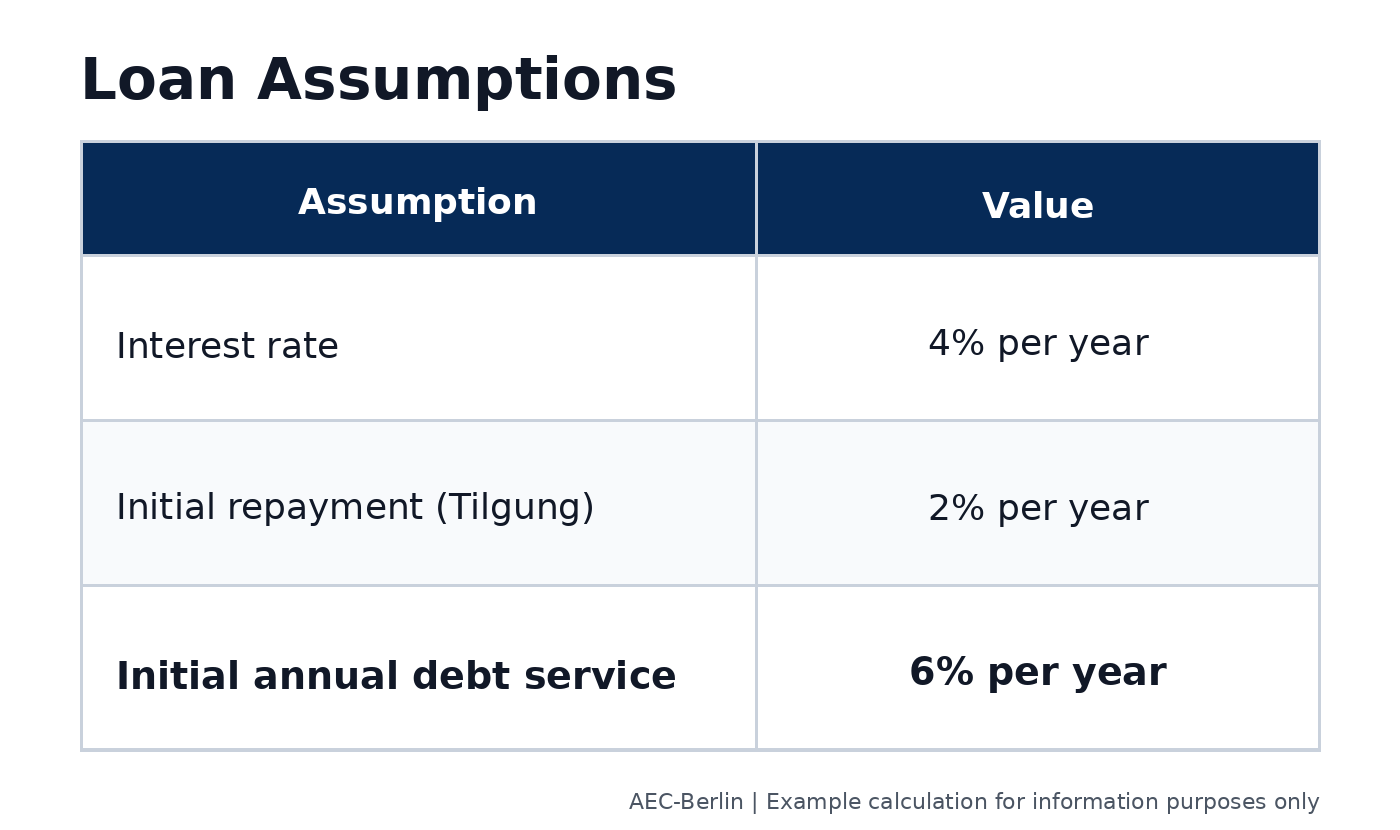

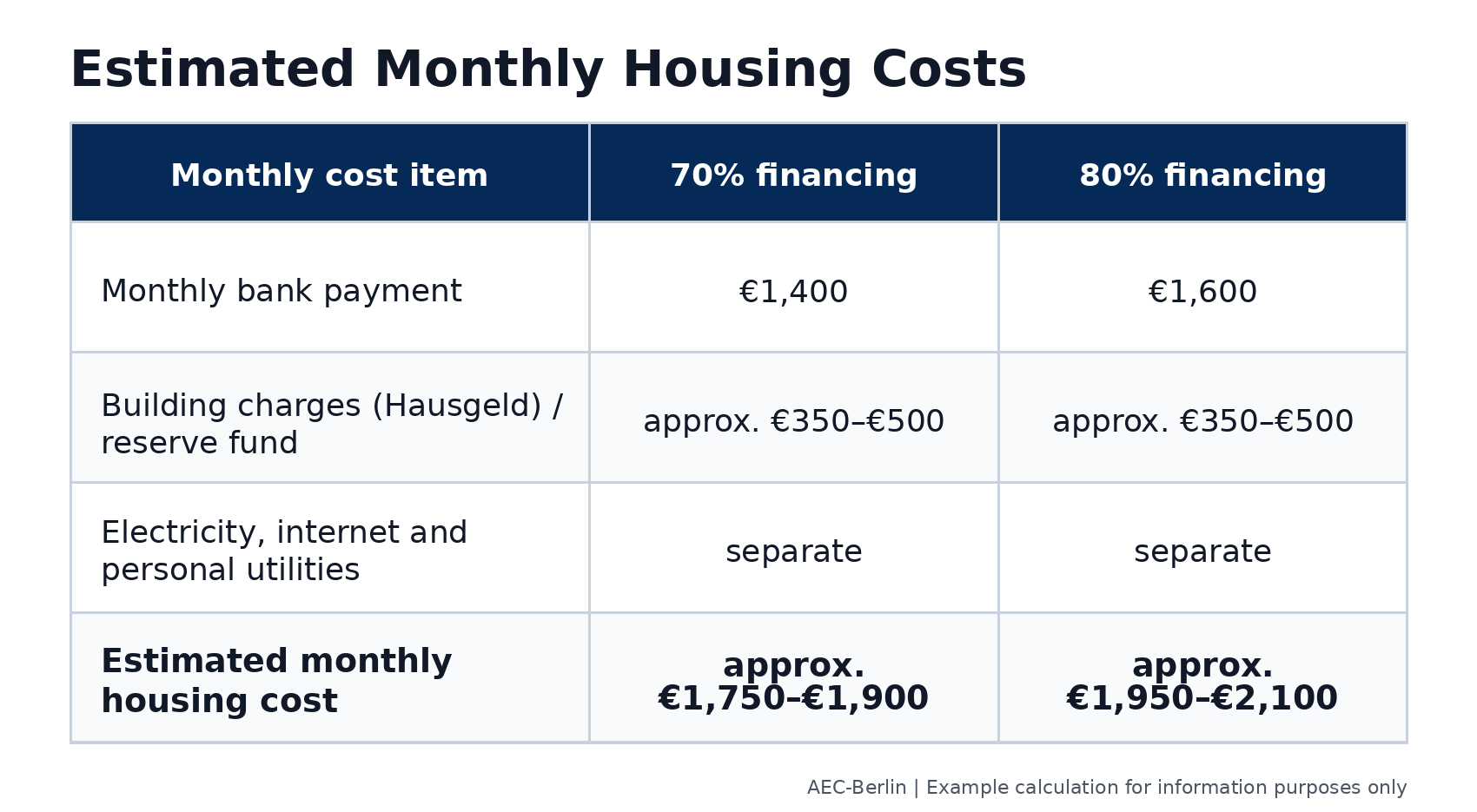

Under this simplified calculation, the initial monthly bank payment would be:

The bank payment is not the only monthly cost. In an apartment building, the owner also pays Hausgeld. This usually includes building management, maintenance reserves and shared building costs. Electricity, internet and personal utility costs are usually paid separately.

This is where the comparison with rent becomes interesting. If a family already pays €1,700–€2,000 per month for a rental apartment, buying may be worth analysing seriously. The monthly burden may be similar, but part of the bank payment is repayment of principal and therefore builds equity over time.

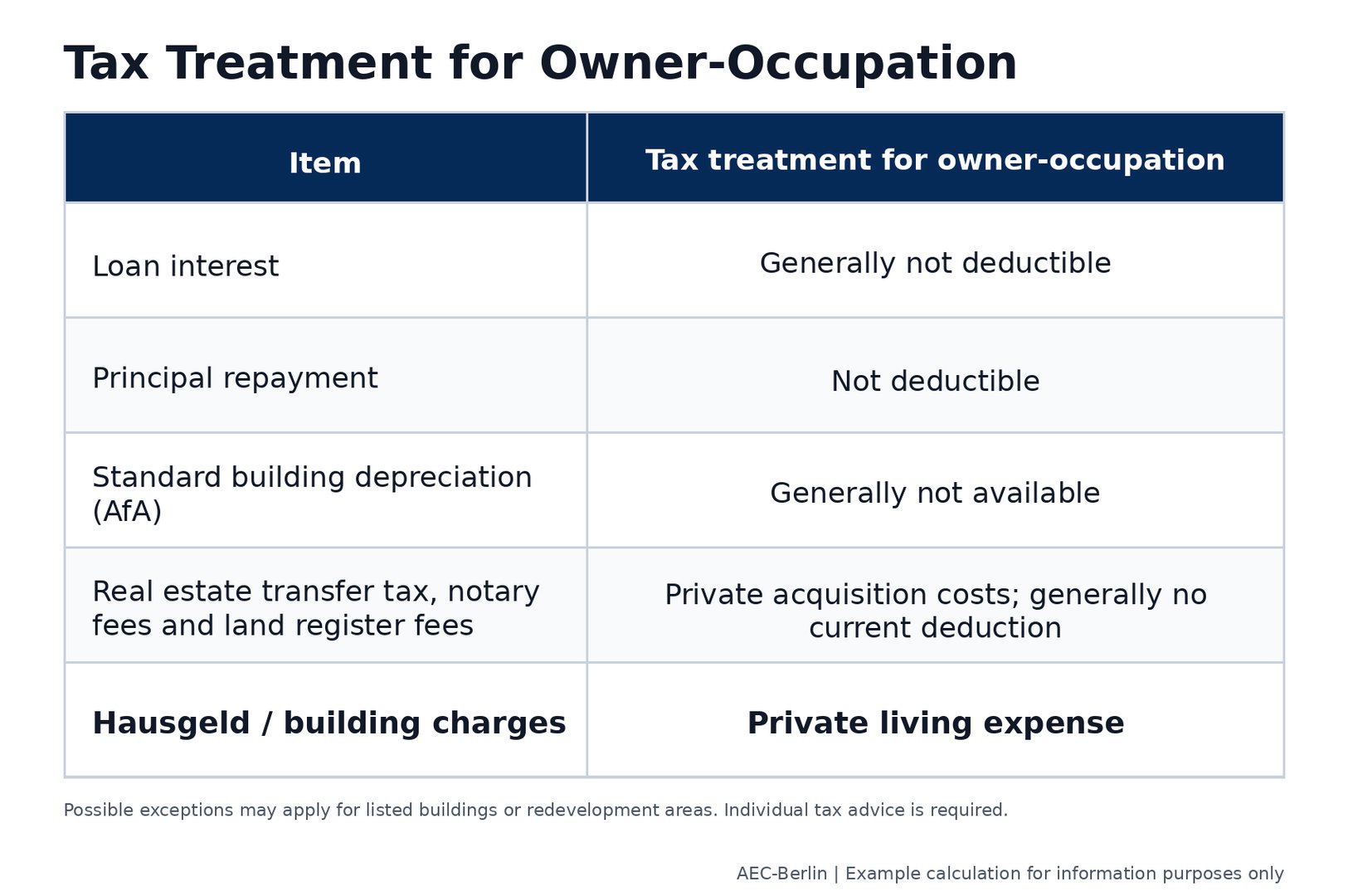

Tax treatment for owner-occupation

International buyers often ask whether they can deduct loan interest, depreciation or purchase costs from their taxes when they live in the property themselves.

In most standard cases, the answer is no. The reason is simple: the owner is not generating taxable rental income from the property. The apartment is used privately.

There can be exceptions for listed buildings, heritage properties or certain redevelopment areas. In such cases, owner-occupiers may qualify for tax relief under special rules, such as Section 10f of the German Income Tax Act. However, this should never be assumed automatically. For heritage or redevelopment properties, the tax treatment should be checked before modernisation work begins. Certificates and approvals may be required, and if the process is handled incorrectly, the tax benefit may be lost.

The major advantage: tax-free sale for owner-occupied property

The strongest tax advantage of an owner-occupied apartment usually does not arise during the holding period, but at the time of sale.

In Germany, a private real estate sale can be taxable if the property is sold within ten years after acquisition. However, there is an important exception for owner-occupied property.

A sale can be tax-free if the property was used for the owner’s own residential purposes either continuously between purchase and sale, or in the year of sale and the two preceding calendar years.

This is often described as the two-calendar-year rule. It does not mean there is a fixed “2.5-year rule”. The decisive point is the actual use of the property and the relevant calendar years.

The owner should also be able to prove actual residence, for example through registration, utility contracts, insurance documents and other evidence.

Why Berlin can be attractive

Berlin remains attractive for many international buyers. It is a large, international city with high housing demand, limited supply in many locations and high construction costs.

Still, property prices do not rise automatically. Interest rates, regulation, location, condition, energy efficiency and market sentiment all matter.

For families planning to stay in Germany, owner-occupied property can therefore be both a lifestyle decision and a long-term wealth-building decision.

Conclusion

Buying an owner-occupied apartment in Berlin can make sense for international families with stable income and sufficient equity. A temporary residence permit makes financing more challenging, but not impossible.

A cautious calculation may use 70% financing, while 80% financing can be realistic for stronger borrower profiles.

The ongoing tax benefits of owner-occupation are limited. Standard depreciation and loan interest deductions are generally not available for a privately used apartment.

The key advantages are different: housing stability, protection against rising rents, equity building through repayment and the possibility of a tax-free sale if the owner-occupation rules are met.

Important note:

This article provides general information only and does not replace legal, tax or mortgage advice. Before purchasing property, buyers should obtain individual advice from a mortgage adviser, tax adviser, notary and, where necessary, a lawyer.

Free Consultation

Have questions about entering the German market? Request a free consultation.

Request Free Consultation