Why the statutory pension may not be enough — and how self-employed professionals and high earners can build a tax-advantaged retirement plan

Alex is 30 years old, single, and works as an IT engineer in Germany. He earns a gross salary of €6,000 per month, or €72,000 per year.

At first glance, this looks like a strong income. And it is. But Alex quickly realizes that earning a good salary in Germany does not automatically mean building wealth.

After taxes and social security contributions, his net income is much lower than his gross salary. He pays rent, living costs, insurance, travel, and other monthly expenses. At the end of the month, he may live comfortably, but he is not automatically financially independent.

This leads to an important question:

Is it enough to simply receive a good salary every month and rely on the statutory pension later?

For many people, the honest answer is: probably not.

The statutory pension is important — but probably not enough

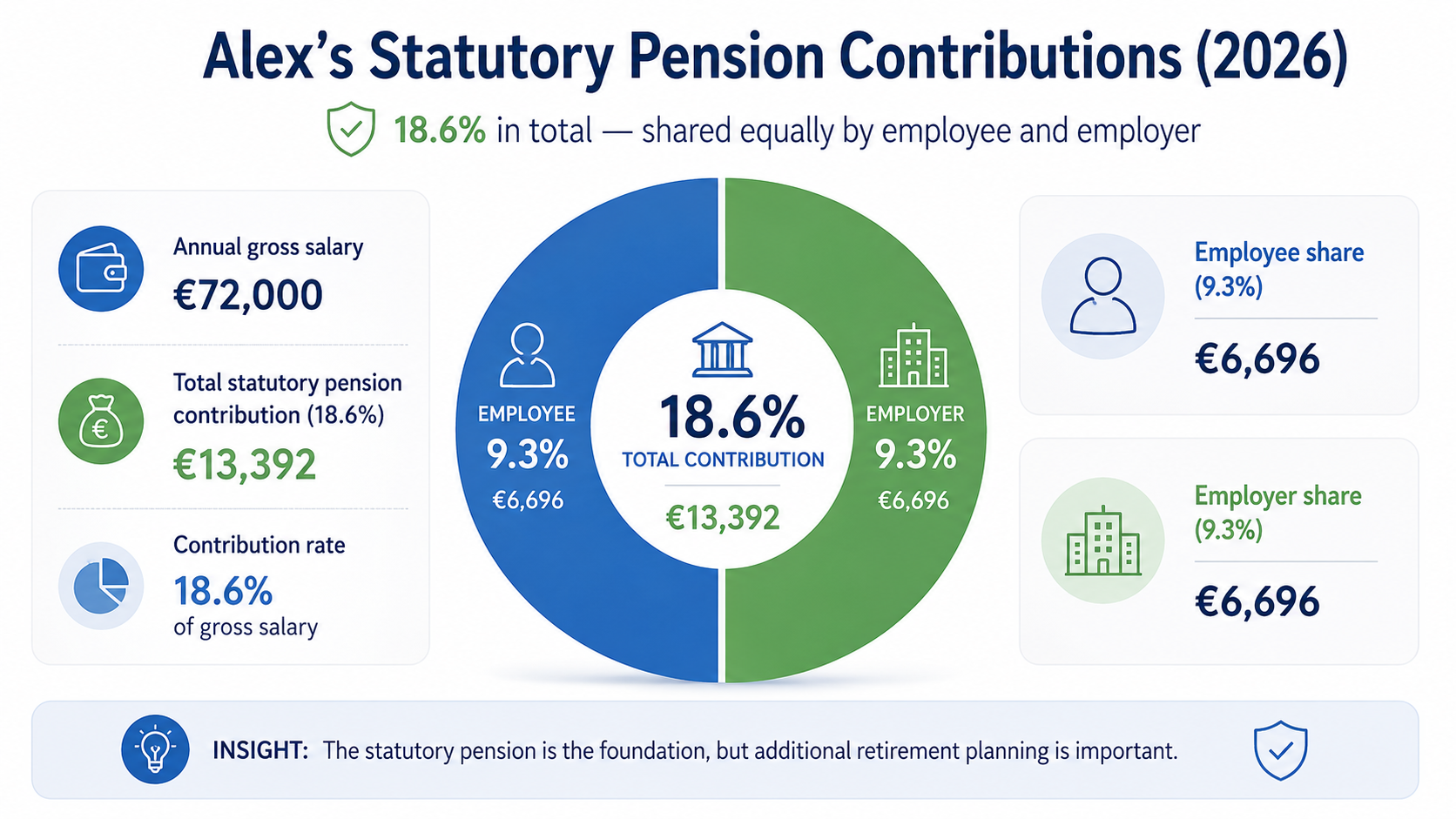

As an employee in Germany, Alex automatically pays into the statutory pension insurance system. In 2026, the contribution rate to the general statutory pension insurance remains 18.6%, split equally between employer and employee, with each side paying 9.3%.

For Alex, this means:

This is a substantial amount. The statutory pension is not meaningless. It is the foundation of retirement provision in Germany.

But it is not designed to fully replace a high professional income.

The German government has extended the so-called pension level guarantee of 48% until 2031. However, this does not mean that every employee will later receive 48% of their last salary as a pension. It is a statistical reference value based on a standard pension compared with average income.

For someone like Alex, who earns €6,000 gross per month and may get used to a certain lifestyle, the statutory pension alone may create a significant pension gap.

That is why the German state encourages additional retirement planning through tax incentives.

Why Germany supports private retirement planning

Germany’s retirement system is under pressure.

People are living longer. The baby boomer generation is retiring. Fewer younger employees will have to finance more pensioners in the future.

This does not mean that the statutory pension system will disappear. But it does mean that employees, self-employed professionals, and high earners should not rely on it as their only retirement plan.

The German state therefore supports additional retirement planning through tax advantages.

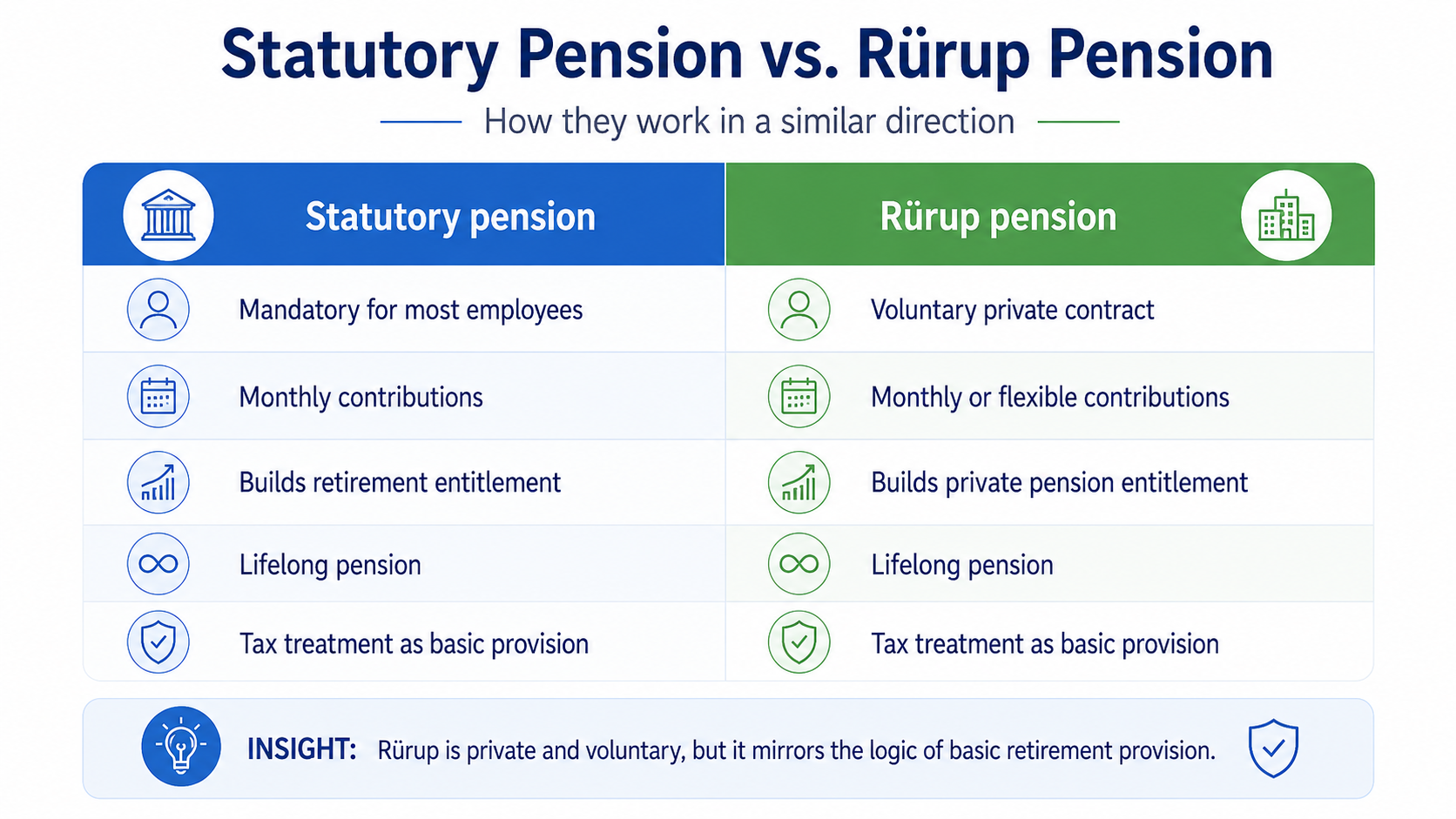

One of the most important instruments is the Rürup pension, also called the basic pension or Basisrente.

What is the Rürup pension?

The Rürup pension is a private retirement contract with special tax treatment.

It belongs to the first layer of German retirement provision, similar to the statutory pension, professional pension schemes, and agricultural pension funds. Contributions to a Rürup pension are treated for tax purposes like contributions to the basic retirement provision. The German Pension Insurance also explains that Rürup contracts are similar to statutory pensions in key restrictions: they cannot be pledged, sold, or transferred.

In simple terms:

Alex pays money into a Rürup pension contract today.

He can deduct these contributions from his taxable income within the legal limits.

Later, in retirement, he receives a lifelong monthly pension.

The pension payments are taxable in retirement.

This is the basic idea of Rürup:

Tax relief today, retirement income tomorrow.

Why Rürup is especially interesting for self-employed people

The Rürup pension was designed especially for self-employed professionals, freelancers, and business owners.

Why?

Because many self-employed people in Germany do not automatically pay into the statutory pension insurance system.

An employee like Alex has pension contributions deducted from his salary every month. His employer also pays a contribution.

A self-employed consultant, software developer, designer, doctor, business owner, or freelancer may not have this automatic pension structure.

That creates a problem:

If the self-employed person does not actively build retirement savings, there may be no sufficient basic pension later.

The Rürup pension can help close this gap.

It works in a similar direction as the statutory pension:

That is why Rürup is often an excellent retirement tool for self-employed people.

It gives them a way to build a tax-advantaged basic retirement pension even if they are not part of the statutory pension system.

The tax advantage in 2026

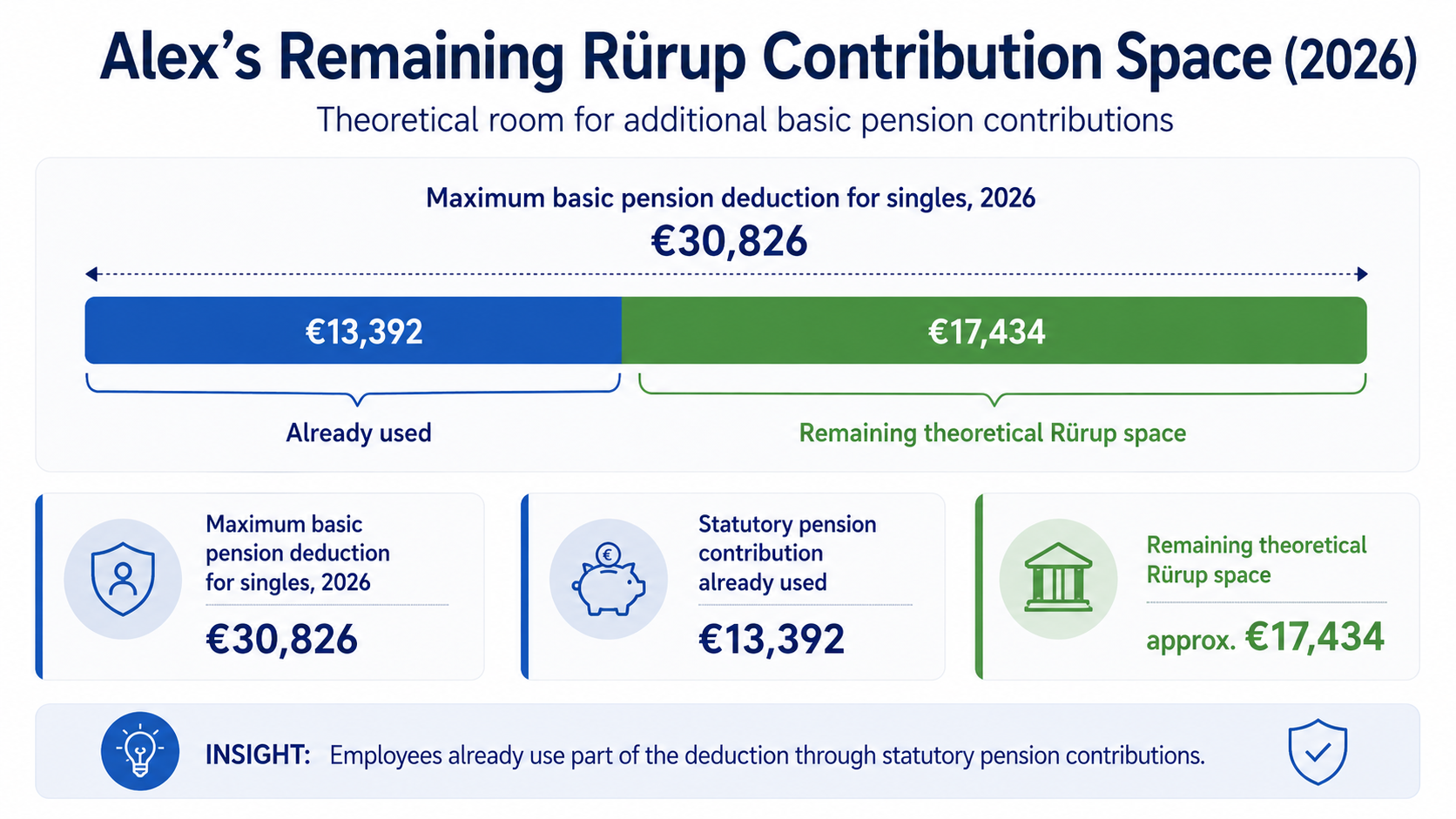

For 2026, the maximum deductible amount for basic retirement contributions is €30,826 for single taxpayers and €61,652 for married couples or registered partners assessed jointly.

This limit includes contributions to the basic pension system, including statutory pension contributions.

For a self-employed person who does not pay into the statutory pension, a much larger part of this limit may still be available for Rürup contributions.

For Alex as an employee, the calculation is different because his statutory pension contributions are already counted.

Alex earns €72,000 per year.

His total statutory pension contribution is approximately:

€72,000 × 18.6% = €13,392

Therefore, his remaining theoretical space for additional basic pension contributions is approximately:

This means that even as an employee, Alex may still have room for additional tax-deductible Rürup contributions.

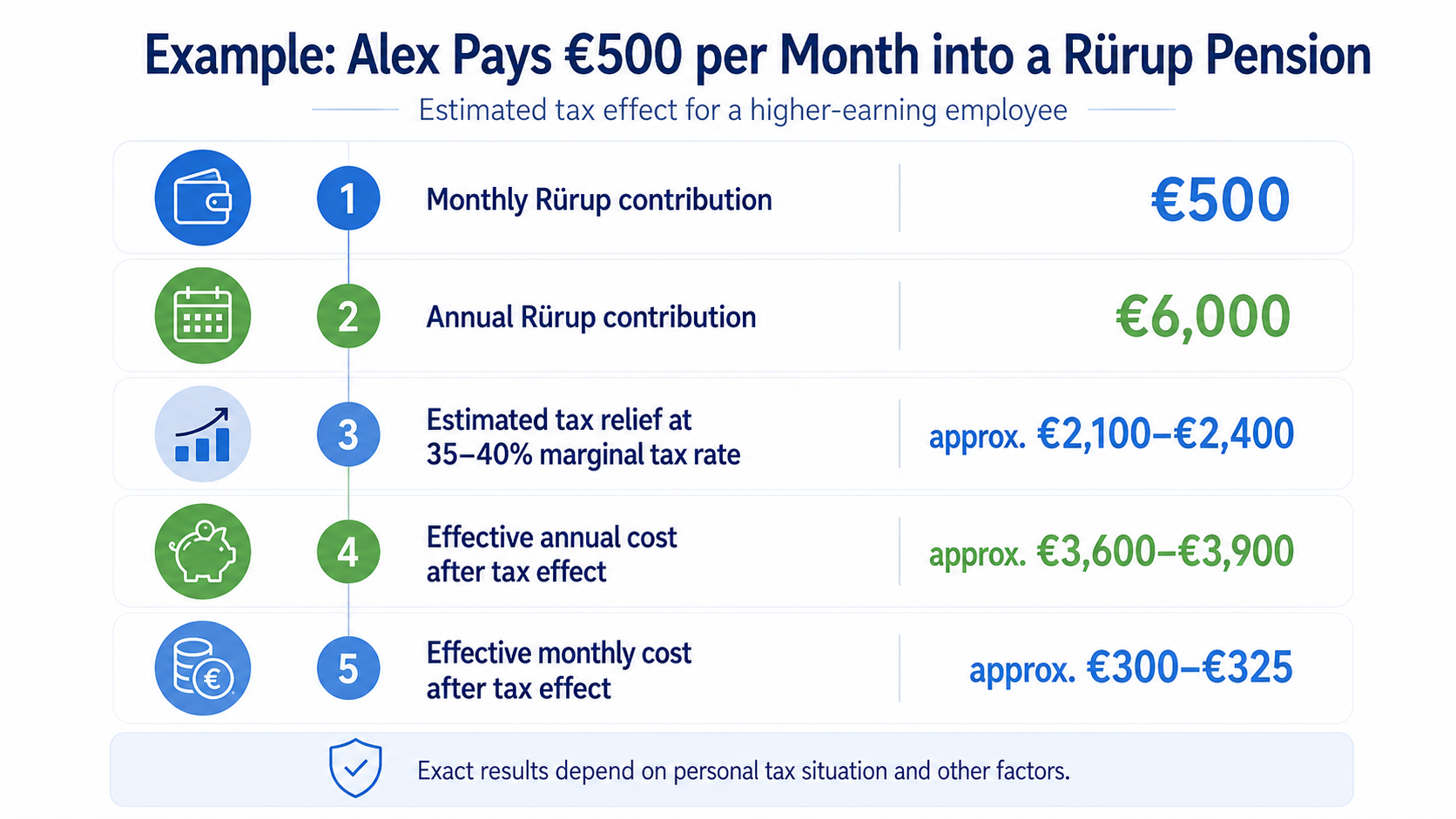

Example: Alex pays €500 per month into a Rürup pension

Let us assume Alex pays €500 per month into a Rürup pension.

This is a simplified calculation. The exact result depends on Alex’s personal tax situation, health insurance status, church tax, deductible expenses, and other factors.

But the principle is clear:

Alex pays €6,000 into his retirement plan.

Because the contribution reduces his taxable income, part of the cost comes back through the tax return.

This is why Rürup can be attractive for people with higher taxable income.

The higher the marginal tax rate, the stronger the immediate tax effect.

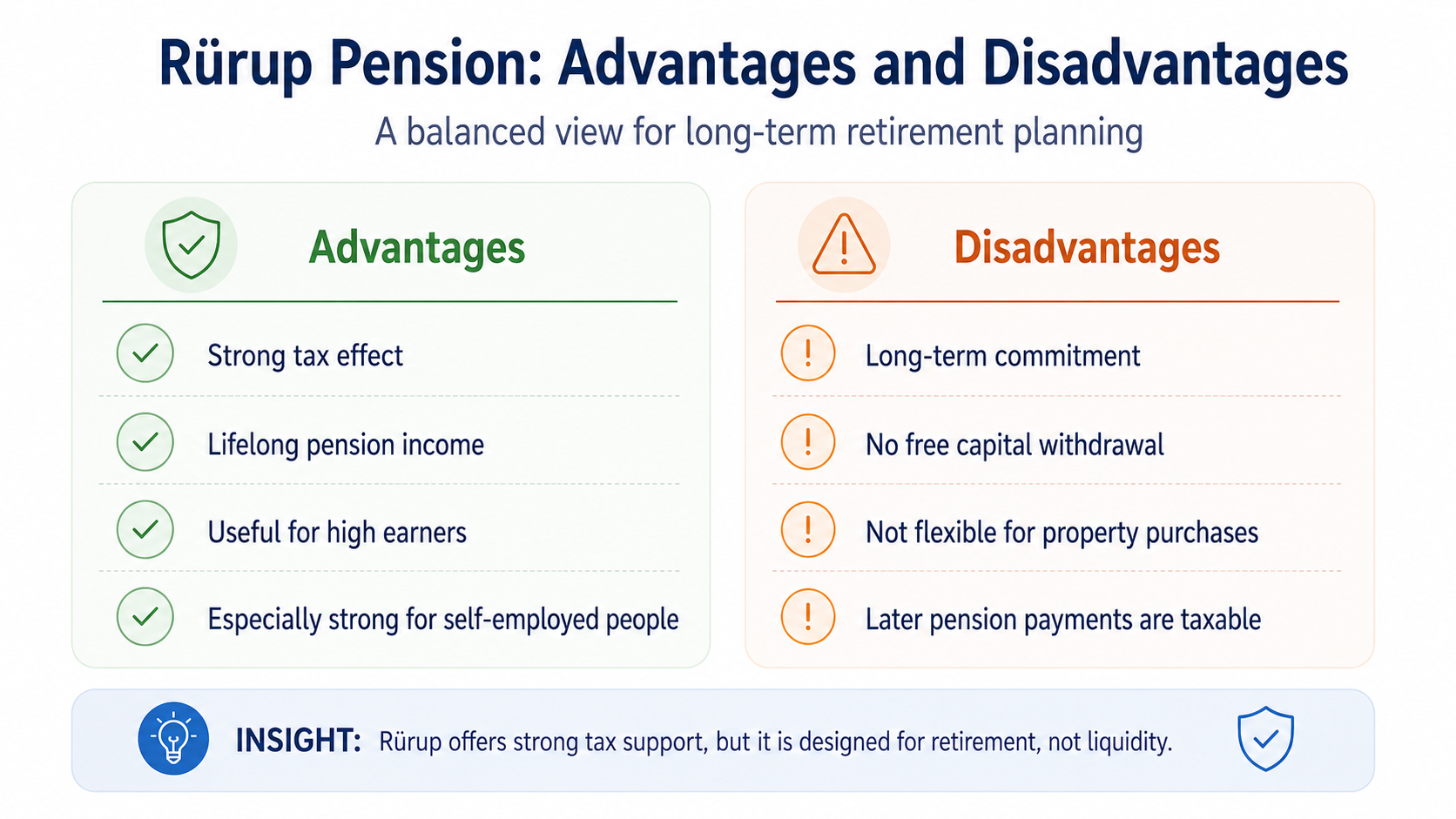

Rürup is not a flexible savings account

The tax advantage comes with restrictions.

A Rürup pension is not like a normal ETF savings plan. Alex cannot simply withdraw the money to buy a property. He cannot use the contract freely as collateral for a bank loan. He cannot treat it like liquid wealth.

This is intentional.

The Rürup pension is designed as retirement provision, not as short-term investment capital.

That means:

Alex should therefore not put all his savings into Rürup.

He still needs liquidity. He needs an emergency fund. And if he wants to buy a rental property later, he needs cash for equity, notary fees, real estate transfer tax, land register fees, possible broker commission, and reserves.

Rürup is not a replacement for liquidity.

It is a retirement pillar.

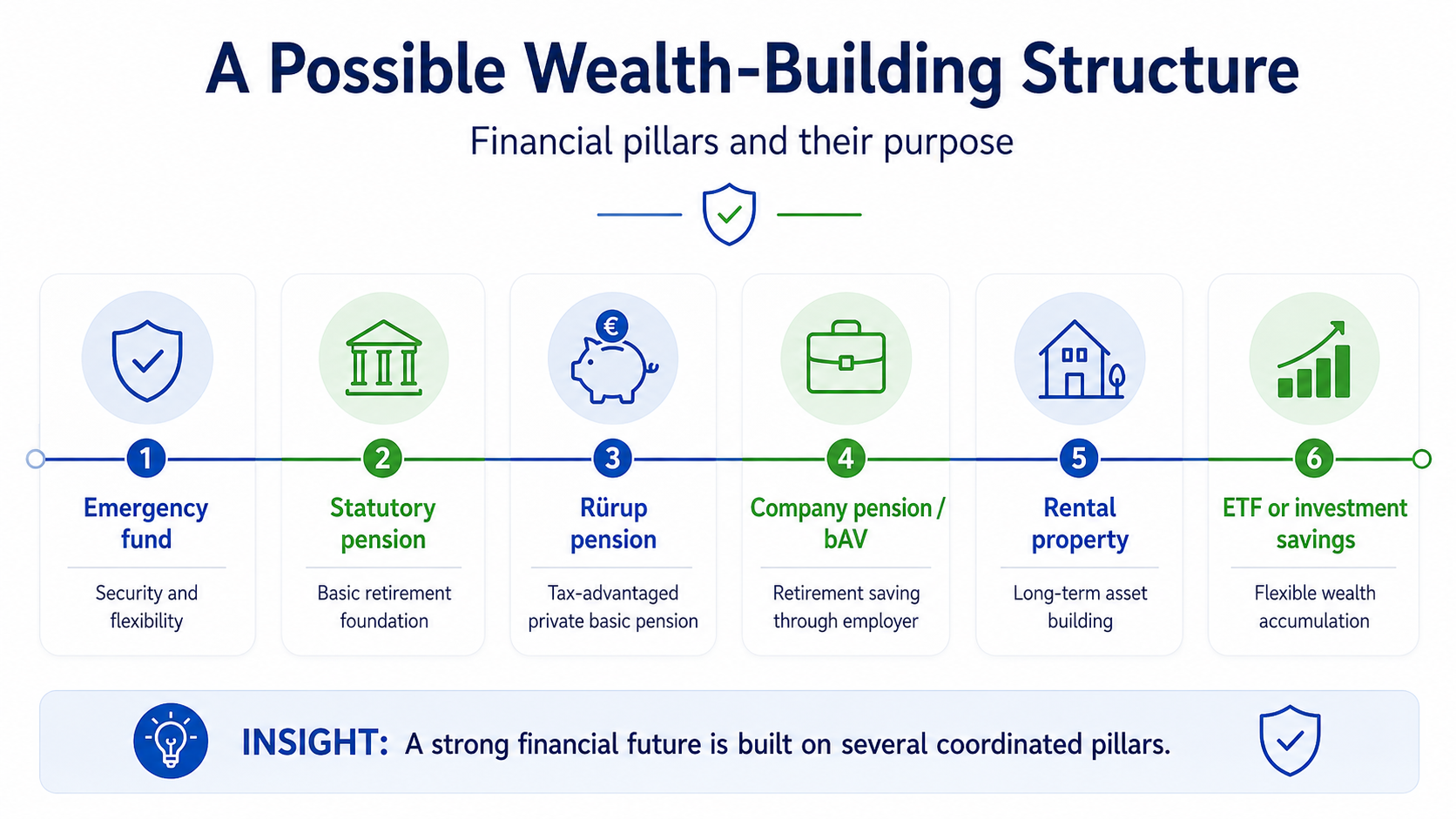

How Rürup fits into Alex’s wealth strategy

Alex should not think in only one category.

The question is not:

Should I buy property or invest in retirement?

The better question is:

How can I structure my income so that I build several financial pillars?

A possible structure could be:

For a self-employed professional, Rürup may be one of the most important tools because there may be no automatic statutory pension contribution.

For an employee like Alex, Rürup can still be useful, especially if he earns well and wants to reduce taxable income while building a long-term pension.

Conclusion: From salary to wealth means building a system

Alex earns good money. But a good salary alone is not a retirement strategy.

The statutory pension is important, but it may not be enough to maintain the lifestyle Alex wants in the future.

The Rürup pension can help him build an additional tax-advantaged retirement pillar. It is especially powerful for self-employed professionals who need an alternative to the statutory pension system. But it can also be attractive for high-earning employees like Alex.

The key is not to chase tax benefits blindly.

The key is to build a balanced structure:

liquidity, tax-advantaged retirement planning, long-term investments, and possibly real estate.

That is how Alex can move from simply receiving a salary in Germany to building long-term wealth.

Important note: This article is a simplified educational example and does not replace individual tax, legal, or financial advice. Rürup contracts differ in costs, guarantees, investment strategy, flexibility, and survivor protection. Each case should be reviewed individually before signing a contract.

Free Consultation

Have questions about entering the German market? Request a free consultation.

Request Free Consultation