Rental property investment in Germany: it is not just about rent

Many international investors look at German property and ask a simple question:

If the rent covers the loan interest, is it a good investment?

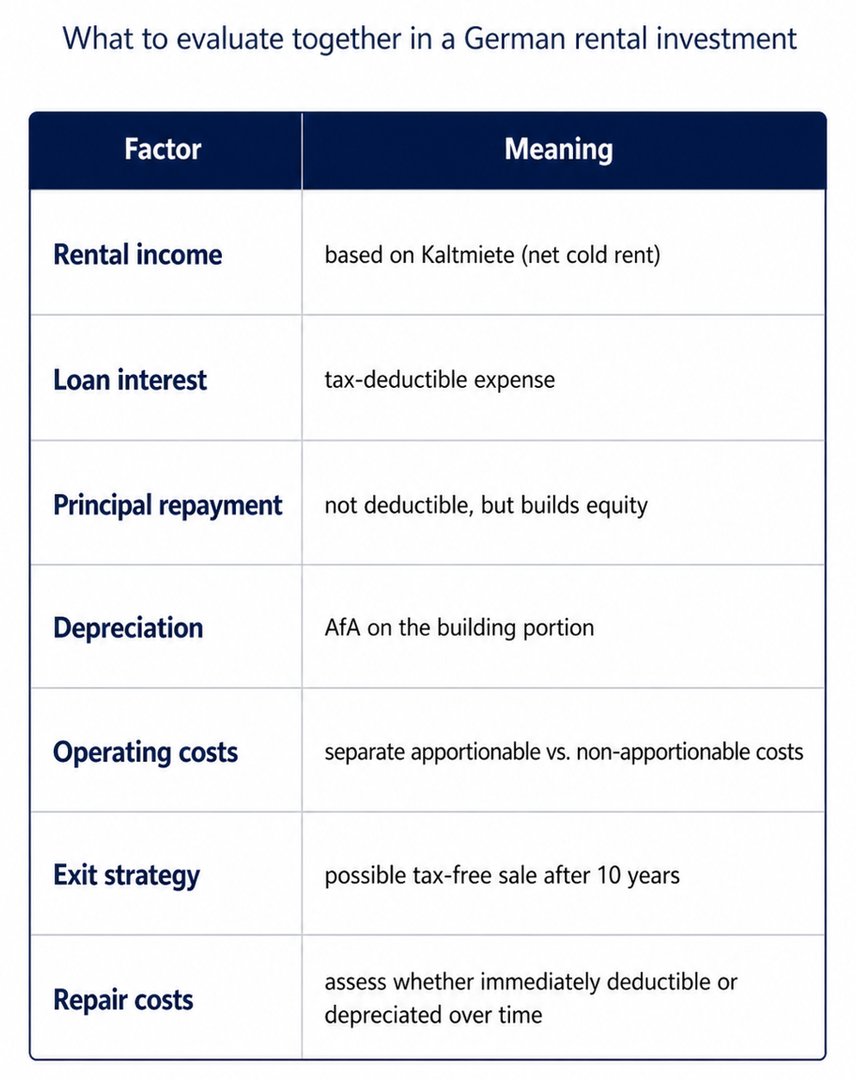

That is a good starting point, but it is not enough. In Germany, a rental property investment should be assessed through several layers: financing, rental income, non-recoverable costs, depreciation, tax effects, repair risks and the exit strategy.

Unlike an owner-occupied apartment, a rental property can generate taxable income from letting. This also means that certain costs can become tax-deductible.

Key factors to evaluate

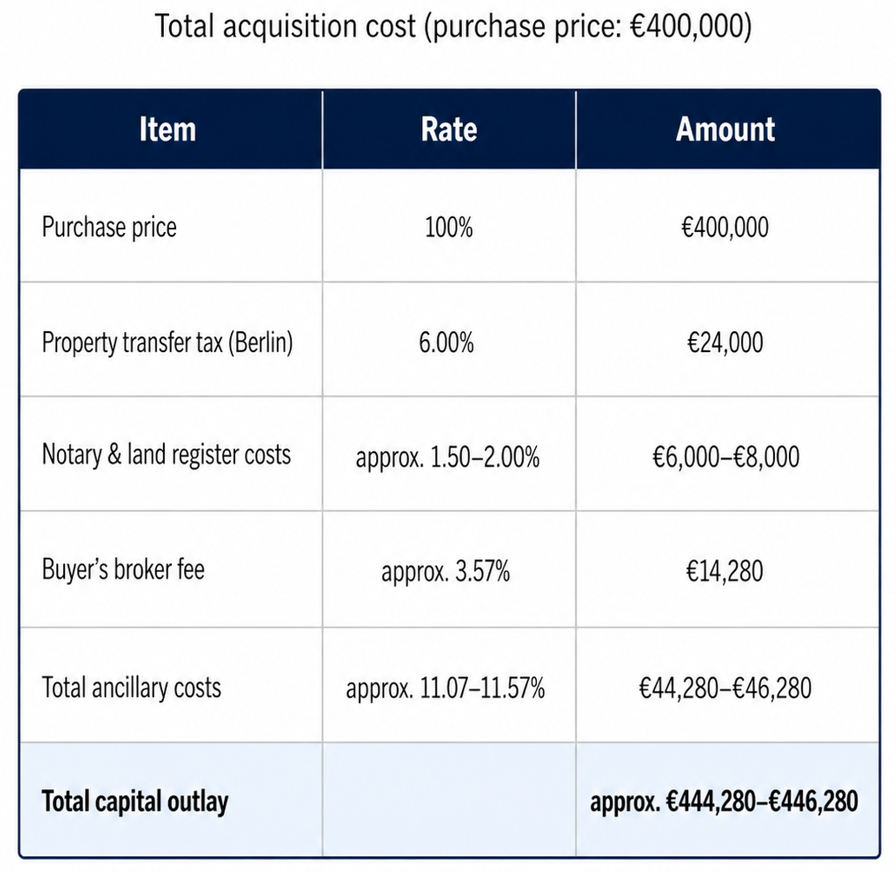

Example: buying a rental apartment in Berlin for €400,000

We use the same example as before: a Berlin apartment with a purchase price of €400,000.

The Berlin real estate transfer tax is currently 6%. For a €400,000 purchase price, this means €24,000.

Because many Berlin apartments are marketed through brokers, the buyer’s broker fee should also be included in a realistic calculation. German law contains special rules for brokerage fees in consumer purchases of apartments and single-family homes.

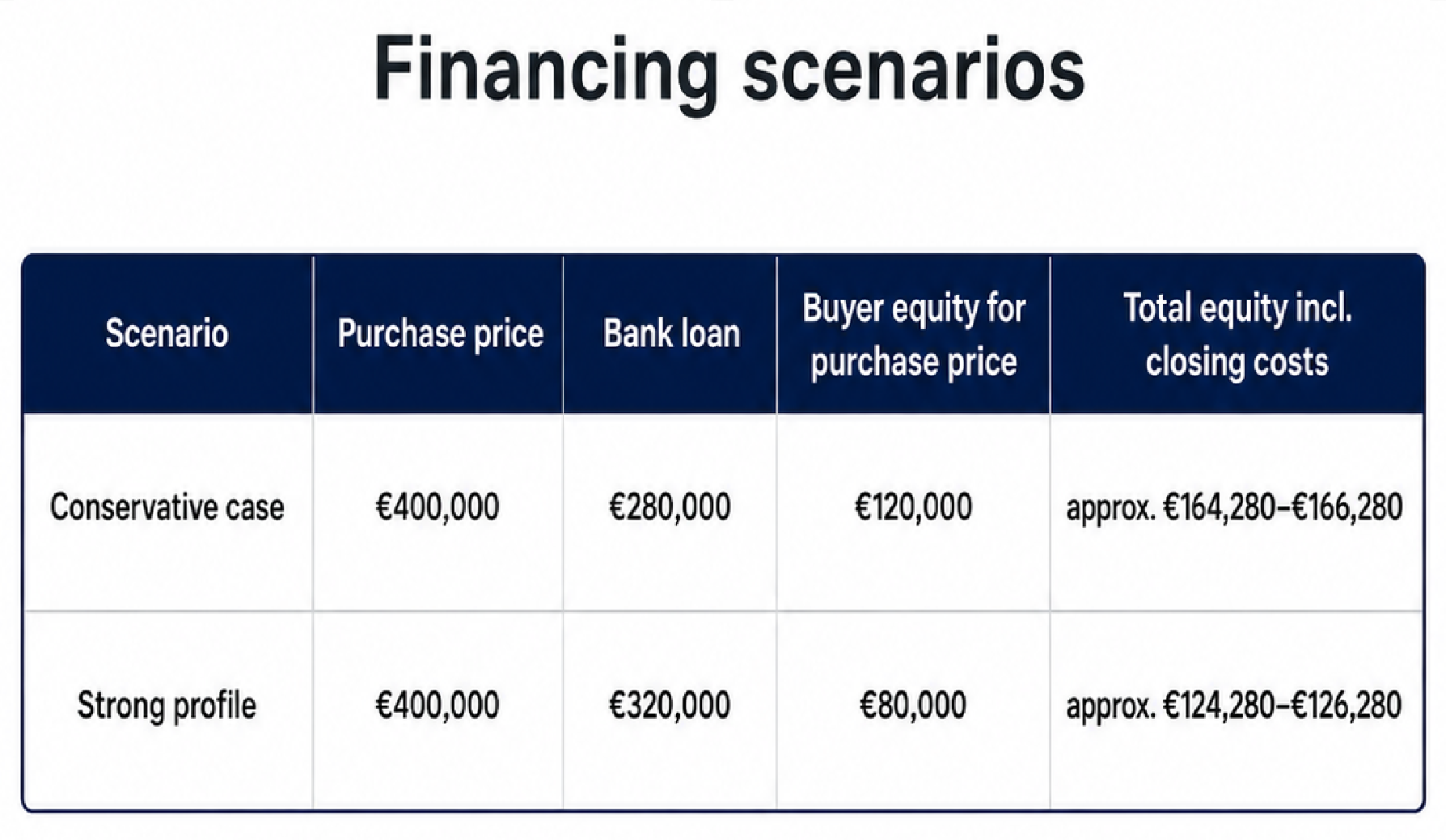

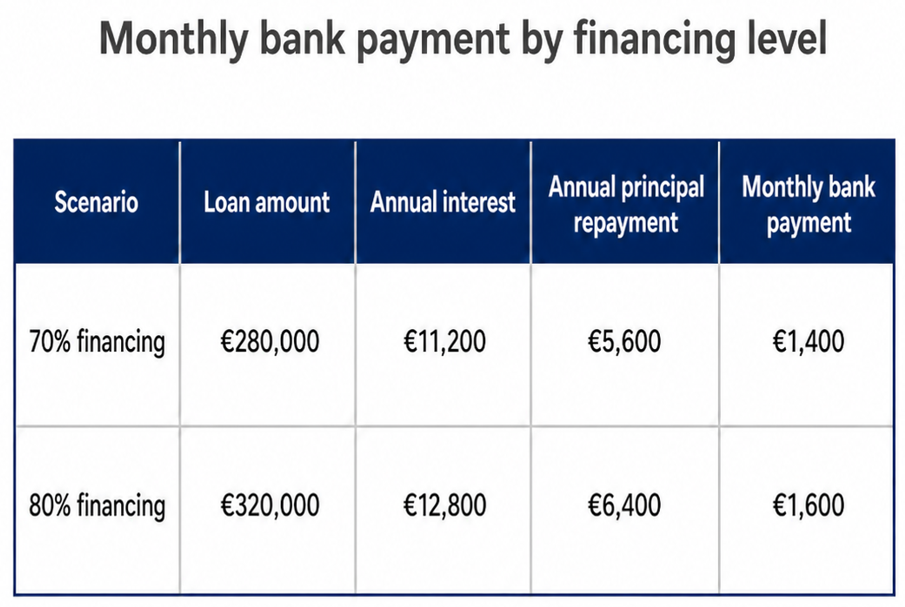

Financing scenarios

International buyers may receive financing in Germany if they have stable income, a valid residence situation, sufficient equity and a property that the bank considers suitable. However, banks may be stricter with buyers who have temporary residence permits or limited German credit history.

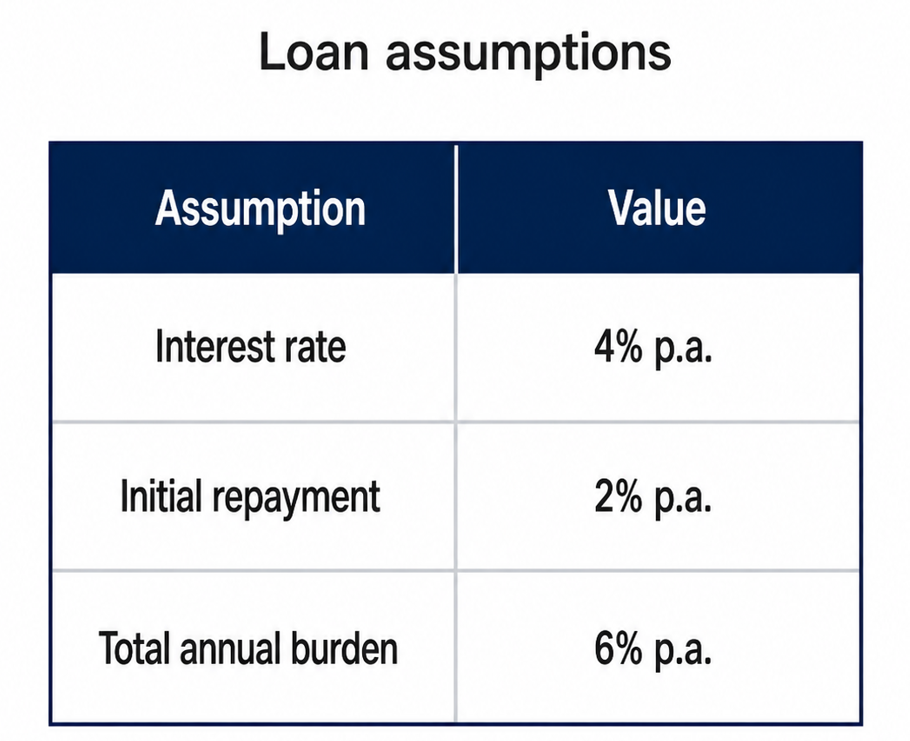

Monthly bank payment

For this example, we use the same loan assumptions:

For tax purposes, the key distinction is that interest can usually be deductible as an expense for rental income, while principal repayment is not deductible. Principal repayment is wealth building, not a tax expense.

Rental income and monthly cash flow

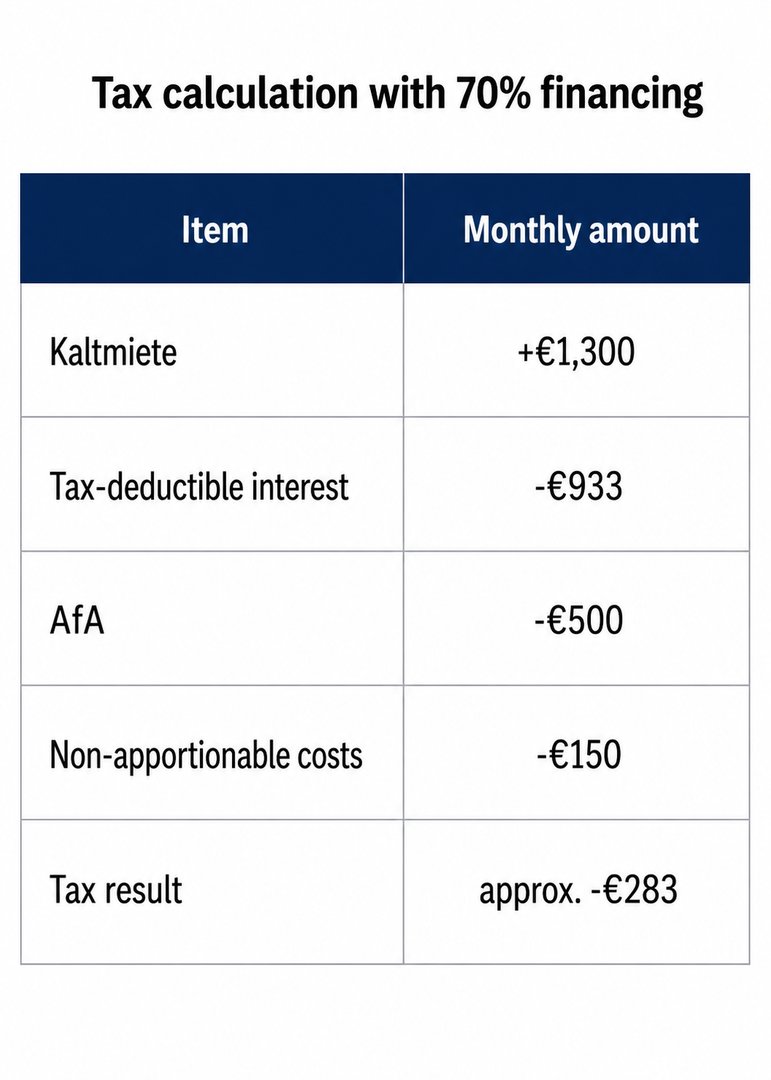

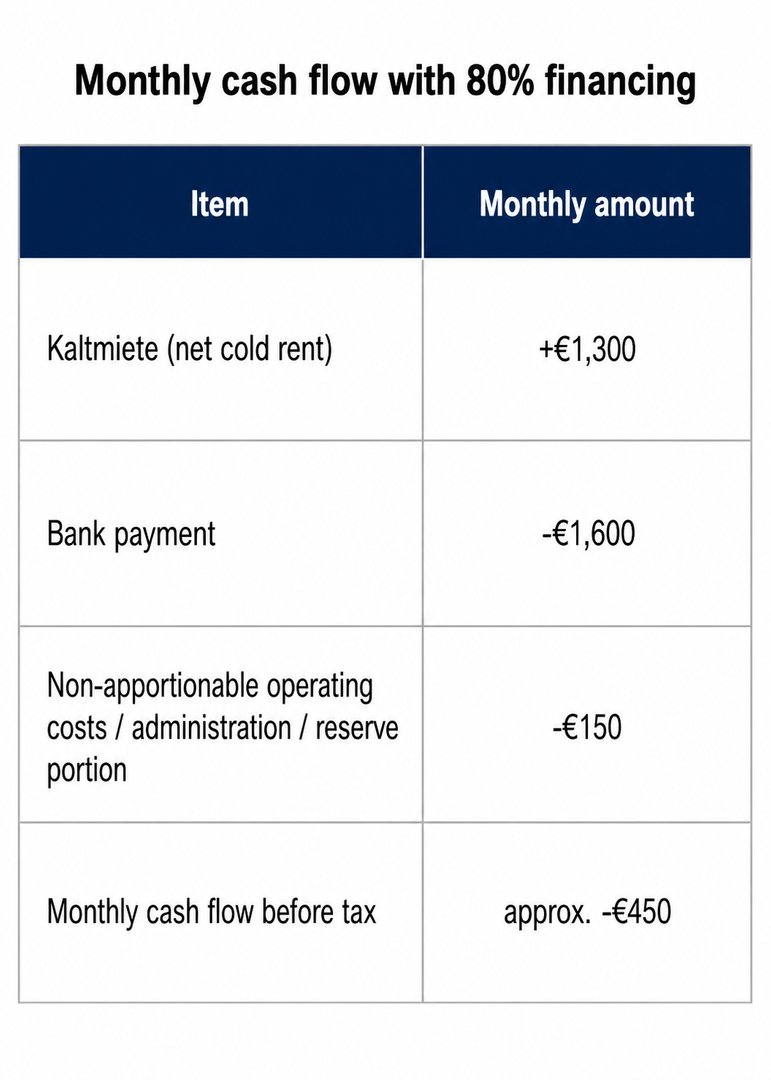

Assume the apartment produces €1,300 monthly Kaltmiete, meaning net cold rent. Also assume the owner has €150 per month in non-recoverable building costs, such as administration or maintenance reserve portions that cannot simply be passed on to the tenant.

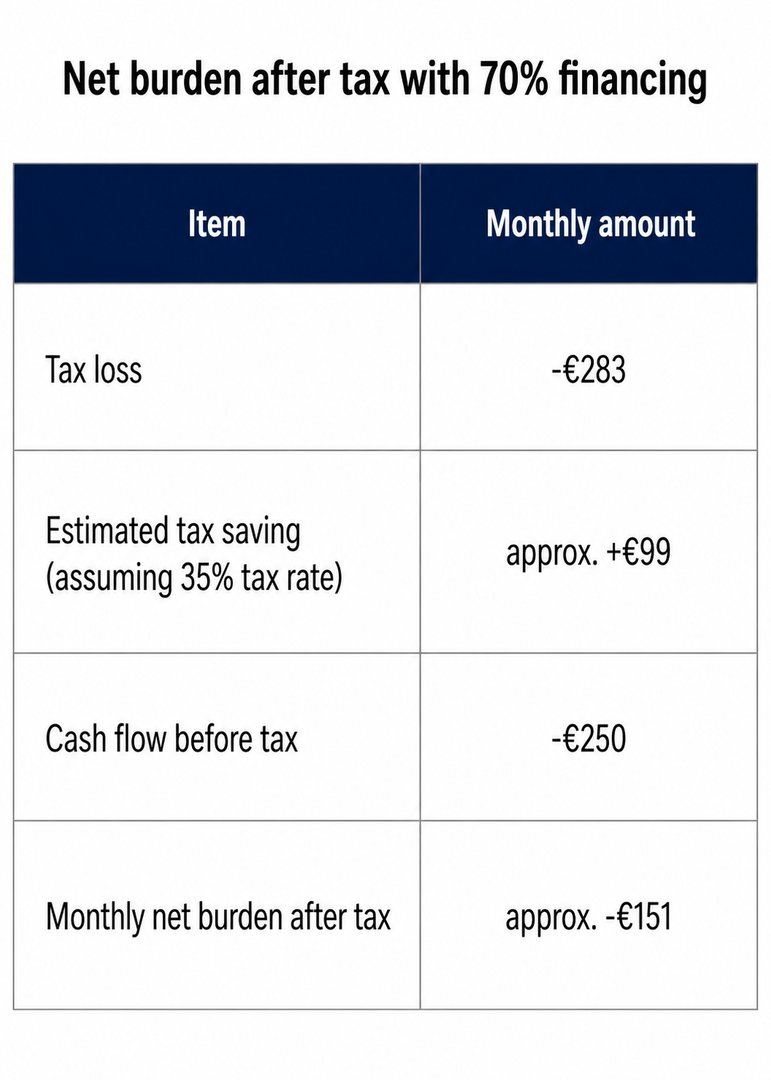

Scenario 1: 70% financing

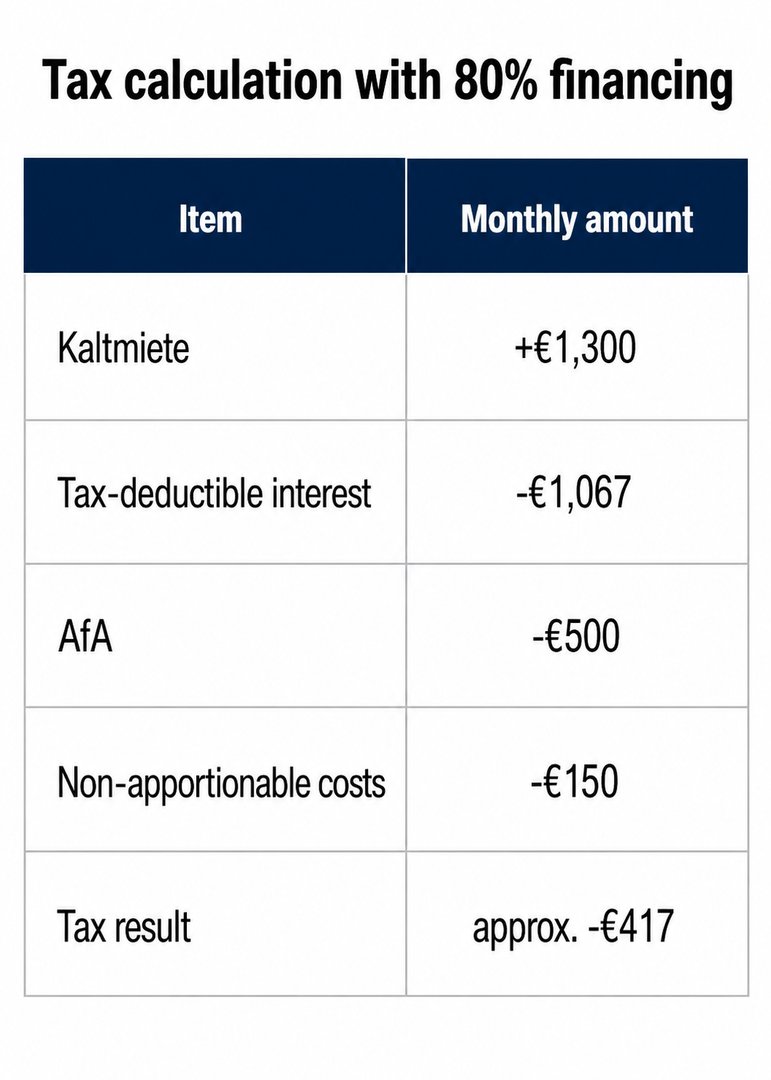

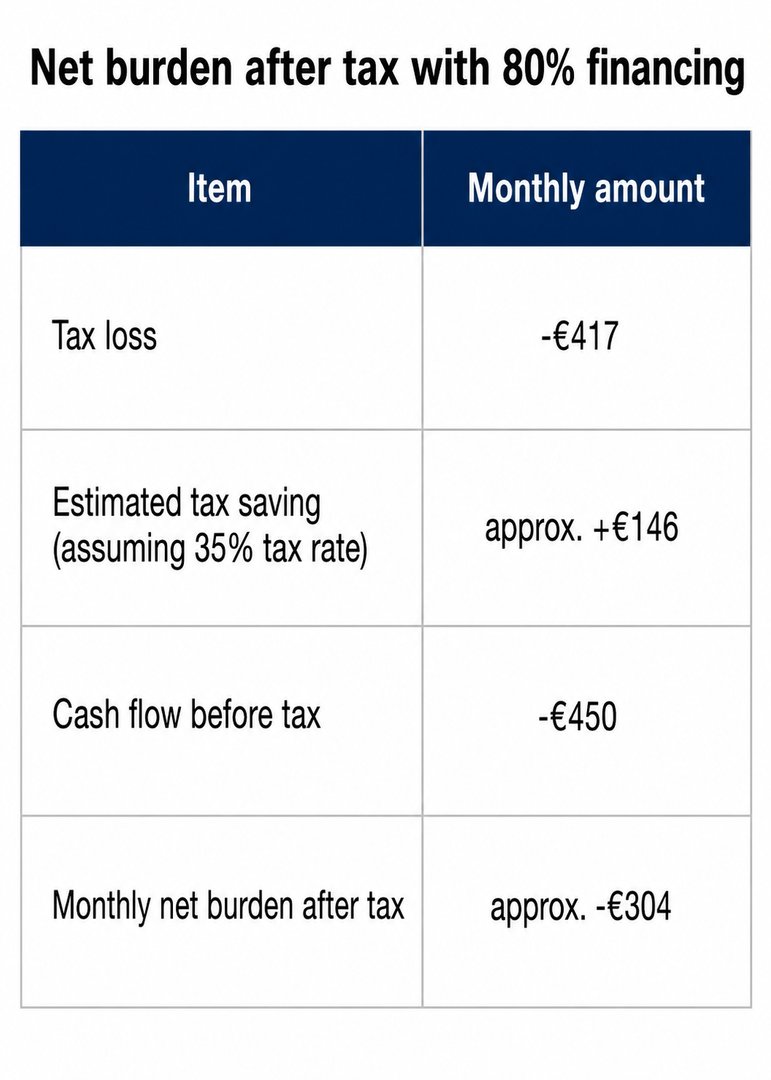

Scenario 2: 80% financing

This shows an important point: a Berlin rental apartment may be attractive in the long term, but it may still create a monthly cash shortfall. The investor must be able to carry this shortfall.

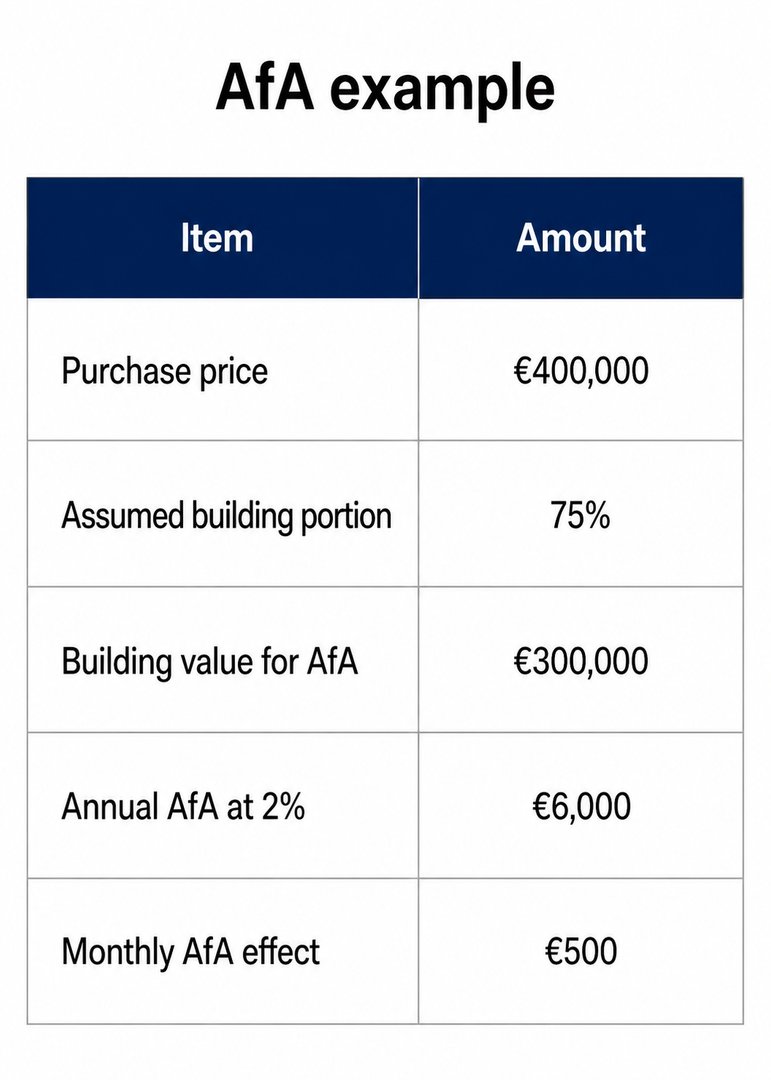

Depreciation: AfA on the building portion

A major tax advantage of rental property is depreciation, known in Germany as AfA.

However, the entire purchase price is not depreciated. Land is not depreciable. Only the building portion can be depreciated. This is why the allocation between land and building value is important.

For many residential buildings, depreciation is commonly 2% per year. For buildings completed before 1925, 2.5% may apply. For newer residential buildings completed after 2022, 3% may apply under Section 7 of the German Income Tax Act.

Example:

The monthly AfA effect is not a cash expense. The owner does not pay €500 per month for depreciation. But for tax purposes, it reduces the taxable rental result.

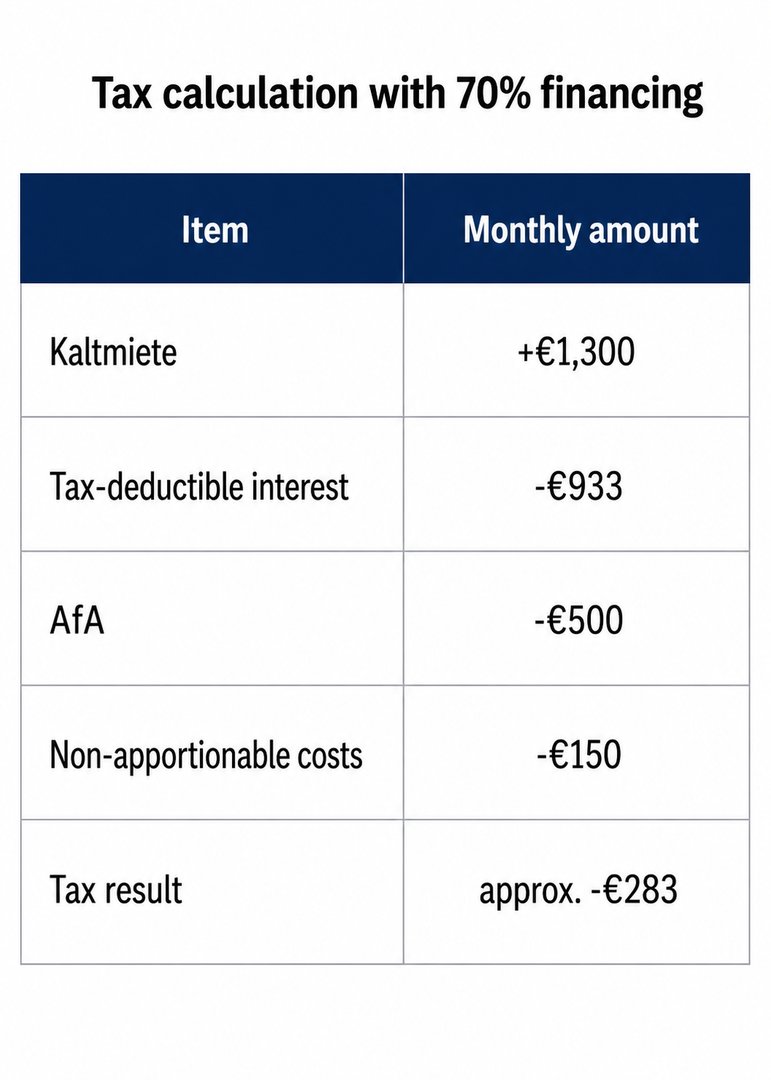

Tax calculation with 70% financing

Although the owner receives rent, the property may show a tax loss because interest, depreciation and non-recoverable costs reduce taxable income.

If the investor’s marginal tax rate is assumed to be 35%, the illustrative tax effect would be:

Tax calculation with 80% financing

With the same assumed 35% tax rate:

This tax effect improves the monthly burden, but it does not replace liquidity planning. The bank payment must still be paid every month.

Are acquisition costs immediately deductible?

Many buyers assume that transfer tax, notary fees, land register fees and brokerage fees are immediately deductible for rental properties. In most cases, this is not correct.

These costs are typically acquisition-related costs. To the extent they relate to the building portion, they increase the depreciation basis and are deducted over time through AfA. To the extent they relate to land, they are not depreciable.

Financing-related costs may need to be treated separately, depending on their nature.

Repair and renovation: the 15% rule

Investors should be careful with repairs and modernisation work shortly after purchase.

German tax law has a rule for so-called acquisition-related production costs. If repair and modernisation expenses within the first three years after acquisition exceed 15% of the building acquisition costs, they may not be immediately deductible. Instead, they may have to be capitalised and depreciated over time. This principle is linked to Section 6 of the German Income Tax Act and is an important risk in tax planning for rental property.

For investors, this means: if major renovation is planned after purchase, the tax treatment should be reviewed before the work begins.

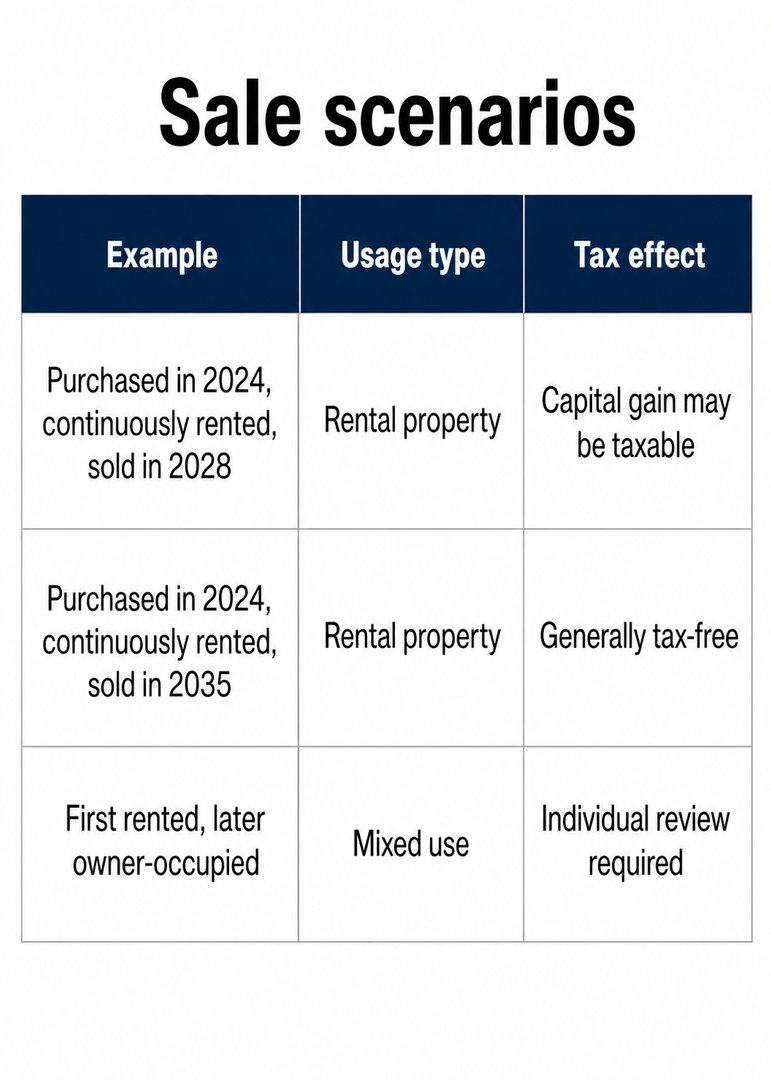

Sale of a rental property: the 10-year rule

For rental properties held as private assets, the 10-year period is crucial. If a rented property is sold within ten years after purchase, the gain may be taxable as a private sale transaction. After more than ten years, a sale of privately held real estate is generally tax-free.

The owner-occupation exception usually does not help if the property was continuously rented, because the property was not used for the owner’s own residential purposes.

What international investors should pay special attention to

First, investors should understand German rental law. Germany has strong tenant protection, and terminating a lease can be much more difficult than in many other countries.

Second, investors should distinguish between Kaltmiete and Warmmiete. Investment calculations should usually be based on net cold rent, because operating cost prepayments are often passed through to the tenant.

Third, the Hausgeld statement should be reviewed carefully. Not all building costs can be passed on to the tenant. The non-recoverable portion matters for cash flow.

Fourth, the minutes of the owners’ association, the WEG, should be checked. Future roof repairs, heating system replacement, elevator work or façade renovation can lead to special assessments.

Fifth, energy efficiency matters. Older buildings can be attractive, but future renovation requirements may affect costs and value.

Sixth, international buyers should consider currency risk if their equity is held outside the eurozone.

Conclusion

Buying a rental apartment in Berlin can be attractive for international investors, but it must be calculated carefully. The key is not simply whether rent comes in every month. The important question is whether the property works after financing, non-recoverable costs, depreciation, tax effects, potential repairs and the exit strategy.

Rental property offers more tax planning opportunities than owner-occupied property. Loan interest, depreciation and certain costs may reduce taxable rental income. However, the monthly cash flow can still be negative, especially with higher financing levels.

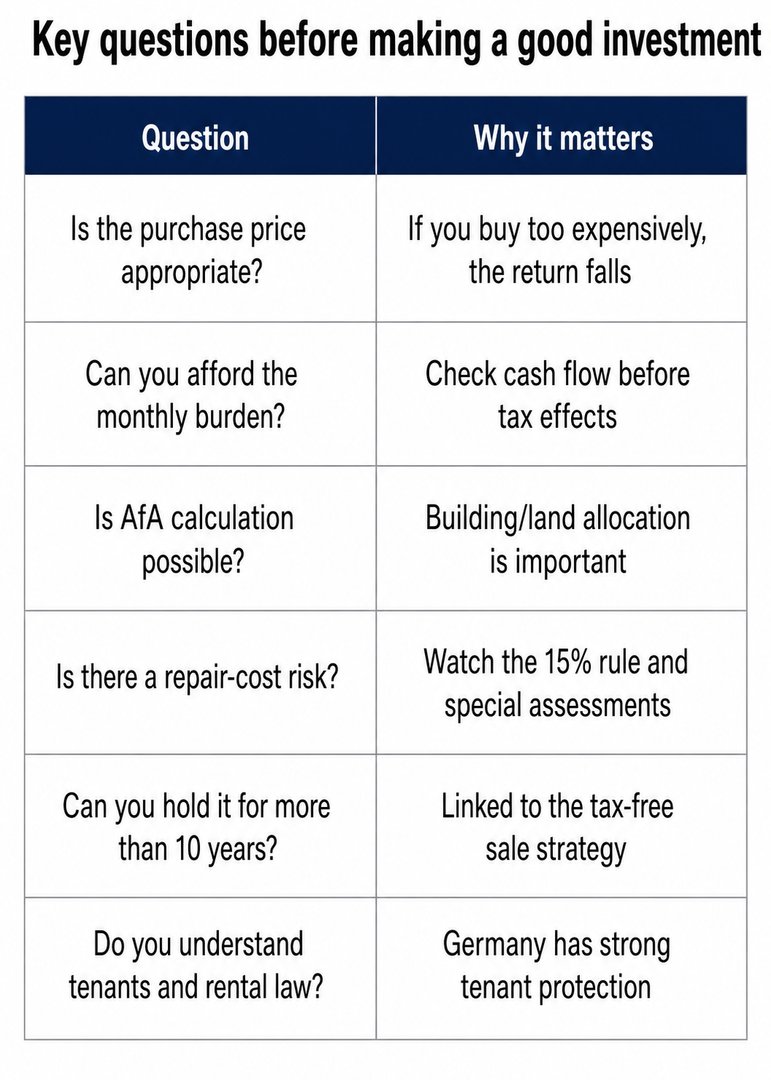

A good rental investment should answer the following questions:

Question

In short:

For owner-occupation, the family’s stability is the central point.

For rental investment, the numbers and the strategy are the central point

Important note: This article provides general information only and does not replace legal, tax or mortgage advice. Before buying a rental property, investors should obtain individual advice from a mortgage adviser, tax adviser, notary and, where necessary, a lawyer.

Free Consultation

Have questions about entering the German market? Request a free consultation.

Request Free Consultation