Which structure is suitable for foreign companies starting business activities in Germany?

Germany is an attractive market for many foreign companies. It is not only one of Europe’s largest economies, but also a strategic gateway to the European Union. For many business owners, Germany offers access to customers, suppliers, technology partners, logistics networks and long-term expansion opportunities within Europe.

However, many foreign companies do not want to establish a full German subsidiary from the beginning.

In many cases, the first step is to test the market: Are there potential customers? Is there demand for the product or service? Can local sales channels be developed? Is it worth building a permanent structure in Germany?

In practice, the term “representative office” is often used for this first phase. The term is internationally understandable, but in Germany it does not describe a separate legal form. What matters is not the name, but the actual activity carried out in Germany.

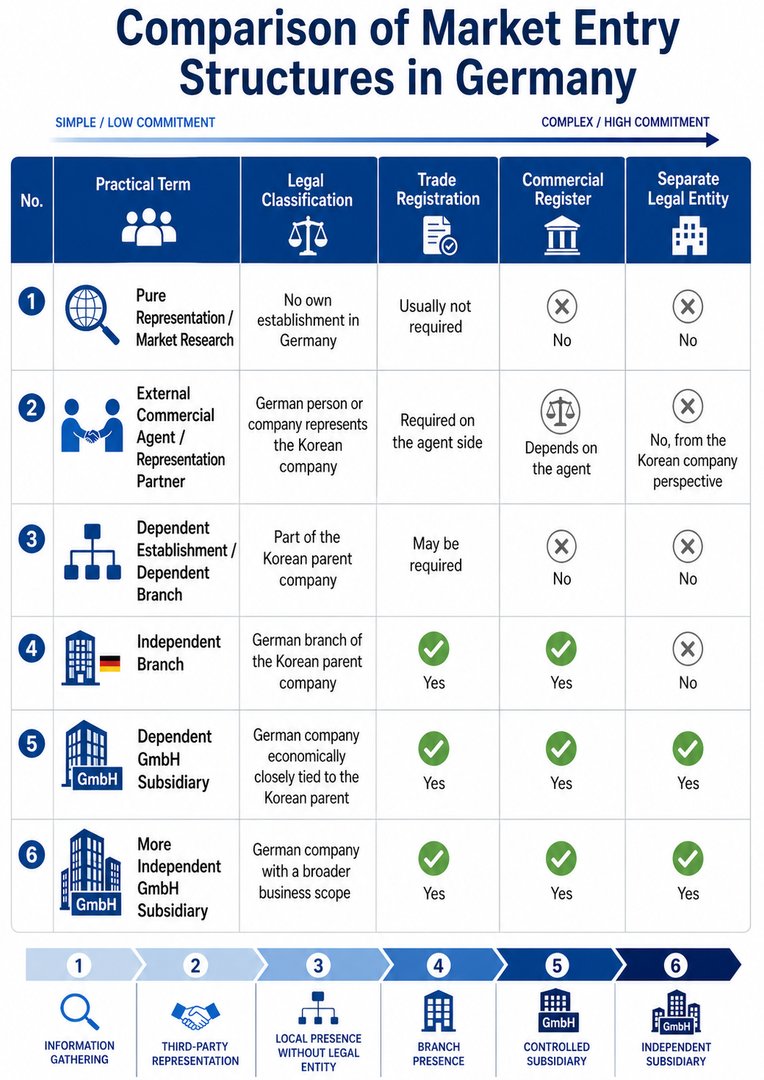

For foreign companies entering the German market, the following practical stages can be distinguished:

1. Pure representation / market research without own establishment in Germany

2. External commercial agent or representation partner in Germany

3. Dependent establishment / dependent branch

4. Independent branch of the foreign parent company

5. German GmbH as an economically dependent subsidiary

6. German GmbH as a more independently operating subsidiary

These structures often develop step by step. A foreign company may first explore the market, then work with a German commercial agent, later establish its own local presence and eventually decide between registering a German branch or founding a German GmbH.

1. Pure representation / market research without own establishment in Germany

The simplest form of market entry is the pure market research or representation phase.

At this stage, the foreign company does not yet have:

a German office,

a German permanent establishment,

a German branch,

a fixed local organization,

local employees in Germany.

Typical activities include:

market research,

trade fair visits,

customer meetings,

search for distributors or sales partners,

first product presentations,

analysis of prices, competitors and demand,

occasional business trips to Germany.

For example, the managing director or an employee of the foreign company travels to Germany, meets potential customers, attends trade fairs and then returns to the home country. Contracts are still concluded abroad. There is no German business address, no German office, no German branch and no local employee of the foreign company in Germany.

In this situation, there is usually no own German establishment yet. Therefore, a trade registration in Germany is generally not required at this early stage.

However, this phase must not be confused with a permanently established German business presence. Once the foreign company creates a fixed business organization in Germany, the legal classification can change.

2. External commercial agent or representation partner in Germany

A practical alternative is to work with an external German partner instead of immediately establishing a German office, branch or subsidiary.

This partner may be:

-an independent commercial agent,

-German UG or GmbH,

-sales agency,

-business development partner,

-representation partner for foreign companies.

In this model, the foreign company itself does not operate as a German establishment. Instead, the German partner provides independent services, sales support or commercial agency services.

Under German commercial law, a commercial agent is an independent businessperson who is permanently entrusted with arranging transactions for another business or, if authorized, concluding transactions in that business’s name.

This means that a German company, such as a UG or GmbH, can generally act as a commercial agent, sales partner or representation partner for a foreign company.

This structure is especially attractive for foreign business owners who want to test the German market without immediately setting up their own German permanent establishment, branch or GmbH.

The structure may look like this:

Foreign parent company appoints German commercial agent / German representation partner for market research, customer acquisition and sales support.

The advantage is flexibility. The foreign company can build customer contacts, test sales opportunities and evaluate market potential before creating its own German organization.

However, the role of the German partner must be clearly defined. If the German partner permanently concludes contracts in the name of the foreign company, negotiates prices with binding effect or effectively acts like a German office of the foreign company, tax questions may arise. In particular, the concepts of a permanent establishment or a permanent representative may become relevant.

Therefore, the agreement with the German partner should clearly regulate:

the scope of services,

-whether the partner may only introduce customers or also conclude contracts,

-whether prices may be negotiated with binding effect,

-whether the partner acts exclusively or non-exclusively,

-how remuneration is structured,

-whether the foreign company remains the contracting party with customers,

-when a German establishment, branch or GmbH should be considered.

3. Dependent establishment / dependent branch

The third stage begins when the foreign company no longer relies only on occasional business trips or an external partner, but starts to build its own local presence in Germany.

The key point is:

Once pure market exploration develops into a permanent German presence with a local organization, the structure should usually be considered a dependent establishment or dependent branch.

Typical indicators include:

-own German office,

-permanently used workplace,

-German business address,

-local representative of the foreign company,

-regular sales activities in Germany,

-own employees in Germany,

-customer support directly from Germany,

-German phone number,

-German business cards or local market presence,

-activities carried out in the name and on behalf of the foreign parent company.

This German presence is not yet a separate company. It remains part of the foreign parent company. No separate German legal entity is created.

Nevertheless, trade registration and tax registration may be required if business activities are actually carried out in Germany.

This structure typically has the following characteristics:

no separate legal entity,

no German GmbH,

no separate liability structure,

no commercial register entry as an independent branch,

but possible trade registration and tax registration in Germany.

In practice, this stage is often the continuation of the initial representation phase. The foreign company has identified Germany as an interesting market and now needs a more permanent local structure.

Special case: foreign employees or company representatives in Germany

A particularly important issue is whether an employee, managing director or representative of the foreign company works in Germany.

If a company representative only travels to Germany occasionally, visits customers, attends trade fairs and then returns to the home country, this does not automatically create a German permanent establishment. Such activity is usually still part of the pure market research or representation phase.

The situation changes if a person works permanently in Germany, supports customers, acquires orders, uses office space or acts as a local representative of the foreign company. In that case, the activity may become a dependent establishment or dependent branch.

It is important to understand that social security status alone is not decisive. A German employee subject to social security contributions is a strong indication of a local presence. But even without German social security, a taxable or registrable German business presence may arise if the activity is permanent and organizationally based in Germany.

Conversely, if a company representative is sent from abroad to Germany only for market research, customer meetings or trade fairs, without a German office, without German employment and without a fixed business facility, a German trade registration is usually not required at the beginning.

However, residence and work permit requirements must also be checked. The distinction between a business trip, assignment, local employment and actual work activity in Germany can be important for immigration law.

4. Independent branch of the foreign parent company

The fourth structure is the independent branch.

In this case, no new German GmbH is founded. The foreign parent company remains the legal entity. The German branch is legally part of the foreign company.

The difference compared to a dependent establishment is the stronger organizational independence.

Typical features of an independent branch include:

own local management in Germany,

own office space,

independent market presence,

separate accounting or organizational structure,

own powers of representation,

German bank account,

permanent business activity in Germany.

An independent branch is registered in the German commercial register. Trade registration is also required. However, unlike a GmbH, the branch is not a separate legal entity.

This means that even if the German branch concludes contracts, the foreign parent company remains the legal entity behind the business.

This structure may be suitable if:

the foreign company wants to operate in Germany under its own name,

the company does not yet want to establish a German GmbH,

but a more formal German structure is needed than a simple representation or dependent establishment.

An independent branch is stronger than a representative office and more clearly organized than a dependent establishment, but it is still not a separate German company.

5. German GmbH as an economically dependent subsidiary

For long-term business activities in Germany, many foreign companies choose to establish a German GmbH.

The GmbH is Germany’s most common limited liability company form. A foreign parent company can hold 100% of the shares in a German GmbH. In that case, the foreign company is the sole shareholder.

However, the key point is:

A German GmbH is always a separate legal entity, even if the foreign parent company owns 100% of the shares.

This is the main difference compared to a branch.

In the case of a branch, the foreign company remains the legal entity.

In the case of a GmbH, a new German legal entity is created.

A German GmbH has:

separate legal personality,

its own managing director,

its own tax number,

its own accounting,

its own financial statements,

its own contracts,

its own bank account,

its own liability structure.

In practice, there is often confusion about whether a German GmbH is “dependent” or “independent” from the foreign parent company.

Legally, the GmbH is always independent. Therefore, the term “dependent GmbH” should be used carefully.

A more accurate description is:

The German GmbH is legally independent, but it can be economically, organizationally and functionally closely connected to the foreign parent company.

Examples:

The German GmbH only sells products of the foreign parent company.

The German GmbH acts as the parent company’s European sales unit.

The German GmbH only provides marketing or customer support.

The company purpose is narrowly drafted.

The GmbH is economically strongly linked to the foreign parent company.

A possible company purpose could be:

Distribution, marketing and customer support for products and services of the foreign parent company in Germany and Europe.

This structure is suitable if the German GmbH is mainly intended to serve as the local sales or service arm of the foreign parent company.

6. German GmbH as a more independently operating subsidiary

The sixth structure is also a German GmbH. Again, the foreign parent company may own 100% of the shares.

The difference is not the ownership percentage, but the company purpose and the actual scope of business.

A more independently operating German GmbH may:

acquire its own customers,

offer its own products or services,

work for third parties,

import and export goods,

develop its own business models,

sell products beyond those of the parent company,

expand into Germany or Europe with its own business activities.

A possible company purpose could be:

Trade, distribution, import and export of goods, provision of consulting, marketing, brokerage and service activities, as well as all related activities, insofar as no special permit is required.

This structure is more flexible and may appear more independent and stable to banks, customers and business partners.

It is especially suitable if the German company is not only intended to act as a sales unit of the foreign parent company, but also to develop its own business activities in Germany or Europe.

Why the company purpose is important when founding a GmbH

When establishing a German GmbH, the notary will not ask whether the GmbH is legally “dependent” or “independent.” Legally, it is always a separate company.

However, the practical structure of the GmbH is very important.

Key questions include:

Who will be the shareholder?

Will the foreign parent company own 100% of the shares?

What is the company purpose?

Will the GmbH only work for the foreign parent company?

May the GmbH also work for other customers?

Will it be a pure sales company or a broader operating company?

Who will be the managing director?

Will a manager be sent from abroad?

Is a local representative in Germany needed?

How broad should the powers of representation be?

Should the GmbH be closely linked to the parent company or operate more broadly?

The company purpose is particularly important.

A narrow company purpose may be suitable if the GmbH will only sell or support the parent company’s products or services.

A broader company purpose is usually better if the GmbH may later develop its own projects, additional customers, new services or other business areas.

Therefore, before founding a GmbH, foreign business owners should not only ask whether they need a German company. They should also define what role this German company should play in the long term.

German bank account and practical business credibility

A German bank account is often one of the most important practical issues.

For a dependent establishment or branch, the bank usually needs to review the foreign parent company in detail. This can involve:

foreign company register documents,

articles of association,

shareholder information,

proof of representation,

translations,

notarization or apostille,

beneficial ownership information.

Preparing foreign documents according to German bank requirements can take time.

A German GmbH is often clearer from the bank’s perspective:

German commercial register number,

German business address,

German articles of association,

German managing director,

clear shareholder structure,

German tax registration.

For this reason, a GmbH is often the more practical and stable solution if the company plans long-term customer contracts, local employees, banking relationships and business activities in Germany.

Employees, family members and EU Blue Card

Foreign companies sometimes want to employ managers, specialists or family members in Germany.

This is not automatically prohibited. However, the employment relationship must be genuine, economically justified and properly documented.

Important points include:

real business need,

realistic job description,

suitable qualification,

market-based salary,

actual work performance,

proper employment contract,

correct payroll processing,

social security registration,

residence permit allowing employment.

If a family member is employed, special care is required. The employment must not be merely formal. The role, qualification, salary and business need must fit together.

For qualified foreign specialists, the EU Blue Card may be an important option. The EU Blue Card is a residence permit for highly qualified employment in Germany.

However, the requirements depend on the job, qualification, salary level and duration of employment. Since thresholds and legal requirements may change, the current requirements should always be checked before applying.

Practical support

For foreign companies entering Germany for the first time, it can be useful to test the market through an independent local representation partner or commercial agent before establishing a German branch or subsidiary.

This allows the company to evaluate customer interest, sales potential, local organizational requirements and administrative procedures before deciding whether to create its own German permanent establishment, branch or GmbH.

Aec-Berlin UG supports foreign companies during this early market entry phase and can also assist with the next steps toward establishing their own German structure.

Conclusion

Entering the German market is not simply a question of opening a “representative office.” In Germany, this term is commonly used in practice, but it is not a separate legal form.

What matters is the actual business activity.

At the beginning, a foreign company may test the German market through business trips, trade fairs and customer meetings. This is usually pure representation or market research without an own German establishment.

Alternatively, the foreign company can work with an external German commercial agent or representation partner. This allows the company to test the market without immediately creating its own German organization.

Once the foreign company creates a fixed German presence with an office, local representative, employees or local organization, the structure may become a dependent establishment or dependent branch.

If the German presence becomes more independent and is registered in the German commercial register, it becomes an independent branch of the foreign parent company.

For long-term business activities, a German GmbH is often the most suitable structure. The foreign parent company may own 100% of the shares. Legally, the GmbH is always a separate German company. Economically, however, it can either be closely linked to the parent company or operate as a broader, more independent German or European business entity.

Foreign business owners should therefore consider both the short-term market test and the long-term legal structure from the beginning.

Legal notice

This article provides general information only and does not replace individual legal, tax, accounting, employment or immigration advice. Before entering the German market, foreign companies should review trade law, tax law, commercial register requirements, employment law, social security, double taxation treaties, residence permits and the specific structure of the foreign parent company.

Free Consultation

Have questions about entering the German market? Request a free consultation.

Request Free Consultation