A practical note for immigrant families planning a new life in Germany

Many families who move to Germany and want to become self-employed think about setting up a GmbH right away.

The idea often sounds logical:

• “A GmbH must be better for getting or keeping a visa.”

• “A GmbH looks more professional.”

• “A proper business in Germany should start as a GmbH.”

This is exactly where many families make an expensive mistake.

I am not writing this as a tax adviser or lawyer.

I am writing this as someone who understands the practical side of German company structures, taxation, and everyday business reality fairly well, and who wants to help immigrant families avoid unnecessary financial pressure at the very beginning.

My main point is simple:

A GmbH is not automatically better for immigration or residence purposes.

And for many ordinary families, starting with a GmbH can create more financial strain, not less.

The common misunderstanding

A lot of people believe that a GmbH is somehow safer or more helpful for official immigration purposes.

In reality, the legal form alone is usually not the decisive factor.

What matters much more is whether:

the business idea is realistic,

the financing is secured,

the plan is economically viable,

and the person running it can do so responsibly and sustainably.

In other words:

It is not the GmbH that makes a business convincing.

It is the substance of the business itself.

This is why many immigrant families should ask a different question first:

How much money will actually remain for the family after taxes, insurance, and business costs?

That question is often far more important than choosing the most formal-looking structure.

Why this matters so much for immigrant families

Families who are new to Germany often face several challenges at the same time:

limited knowledge of the German tax system,

language barriers,

difficulty communicating with tax advisers,

uncertainty about health insurance,

high living costs,

and pressure to make the business work quickly.

If a family starts with a GmbH too early, the burden can become much heavier than expected.

A GmbH may bring:

more bookkeeping complexity,

annual financial statements,

more formal obligations,

disclosure requirements,

higher tax adviser costs,

and more room for mistakes.

For a well-capitalized or fast-growing business, a GmbH can make sense.

But for a normal family that needs business income to pay rent, insurance, food, and school-related costs, the situation is very different.

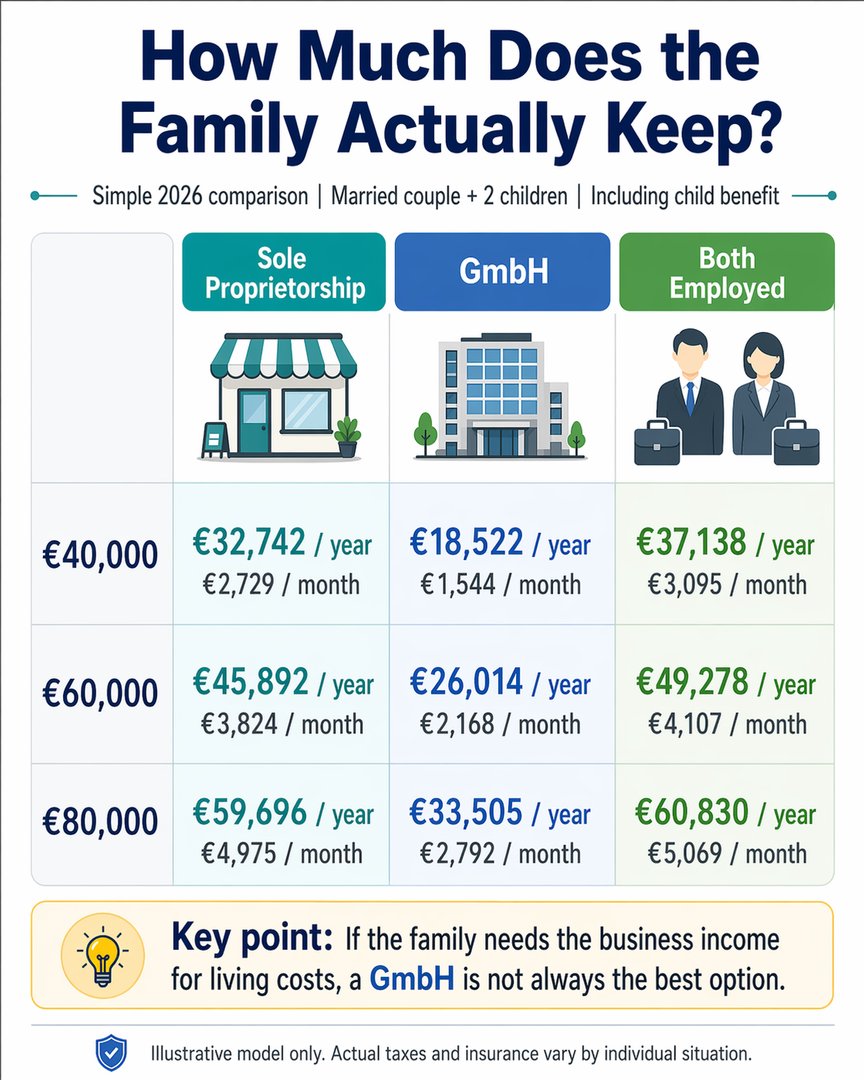

A simple example

To make the issue easier to understand, let us look at a very simple model case.

We compare three family situations:

1) Sole proprietorship

The husband runs the business, and the wife only helps.

Both are voluntarily insured under the public health insurance system.

2) GmbH

The husband runs the GmbH, and the wife only helps.

Both are voluntarily insured as well.

For this example, we use the simple standard model: the company earns a profit, pays company taxes, and the remaining amount is distributed to the husband.

3) Both spouses employed

Both husband and wife work as employees and are covered through the normal statutory system.

Assumptions:

married couple,

2 minor children,

joint tax assessment,

child benefit included,

simplified 2026 model,

no church tax.

Comparison table:

What this example shows

The table does not mean that a GmbH is always bad.

It simply shows that for a family that needs business income for everyday living, a GmbH is often not the strongest starting point.

Why?

Because with a GmbH, money can be reduced at several stages:

tax at company level,

tax when profits are distributed,

health insurance effects depending on personal structure,

plus more administrative and adviser costs.

By contrast, a sole proprietorship is often easier to understand and easier to manage in the beginning.

And if both spouses are employed, the family often ends up with the most stable private household result, because the social insurance structure is simpler and partly shared through employment.

The real danger

The real risk is not just taxation.

It is misjudging the full burden.

Many immigrant families underestimate:

voluntary health insurance costs,

tax adviser fees,

accounting stress,

filing deadlines,

and the emotional pressure of dealing with German bureaucracy while trying to build a new life.

That is why the issue is not only legal or tax-related.

It is also about family stability.

A company structure that looks professional on paper may still be the wrong choice if it pushes a family into financial stress within the first year.

When a GmbH can still make sense

A GmbH can absolutely be the right choice in some situations, for example:

if liability protection is especially important,

if there are multiple founders,

if profits will stay inside the company for reinvestment,

or if the business is already operating at a larger scale.

So this is not an anti-GmbH argument.

It is simply a warning against starting with a GmbH for the wrong reason.

My advice to immigrant families

Before choosing a business structure, ask these questions first:

How much money does our family need every month?

How much will remain after tax and insurance?

Can we survive the first 6 to 12 months if income is lower than expected?

Can we realistically manage bookkeeping and compliance?

Are we choosing a GmbH for real business reasons, or only because it sounds safer for immigration?

Those questions are often more important than the legal form itself.

Final thought

Germany offers real opportunities.

But for immigrant families starting from zero or near zero, the best start is often not the most complicated structure, but the one that is easiest to understand, easiest to manage, and most sustainable for daily life.

So my message is simple:

Do not assume that a GmbH is automatically better for immigration.

First calculate what your family can actually keep.

A simpler structure may be the safer beginning.

Disclaimer

This article is not tax or legal advice. It is a general explanatory model meant to help families understand the practical differences between common business situations in Germany. Actual taxes, health insurance contributions, and legal outcomes depend on the individual case.

Free Consultation

Have questions about entering the German market? Request a free consultation.

Request Free Consultation