How employees can use bAV, Direktversicherung, and employer subsidies to build additional retirement wealth

Alex is 30 years old, single, and works as an IT engineer in Germany.

He earns €6,000 gross per month, or €72,000 gross per year.

He has a good job, a stable salary, and strong career prospects. But he also understands one important truth:

A salary is not the same as wealth.

A salary pays monthly bills. Wealth is built when part of that income is systematically converted into assets.

For an employee in Germany, one of the most practical tools for this is the company pension, known in German as betriebliche Altersvorsorge, or bAV.

One of the most common forms of bAV is the Direktversicherung, or direct insurance.

The method used to fund it is often called salary conversion or Entgeltumwandlung.

Why Alex should not rely only on the statutory pension

Like most employees in Germany, Alex automatically pays into the statutory pension insurance system.

In 2026, the general statutory pension contribution rate is 18.6%, split equally between employer and employee.

At Alex’s salary level, this means that a significant amount is already going into the pension system every year.

But the statutory pension is still only the foundation.

The German government has extended the 48% pension level guarantee until 2031, but this does not mean that Alex will later receive 48% of his last salary. It is a reference value for the pension system, not an individual promise for every employee.

For someone who earns €6,000 gross per month, the future statutory pension may be far below the income level needed to maintain the same lifestyle.

That is why Alex should start building additional retirement wealth while he is still young.

What is salary conversion?

Salary conversion means that Alex gives up part of his gross salary and uses it for company pension contributions.

The important point is:

The money is not first paid out as net salary.

Instead, it is transferred directly from gross salary into a company pension contract, for example a Direktversicherung.

This creates a tax and social security advantage.

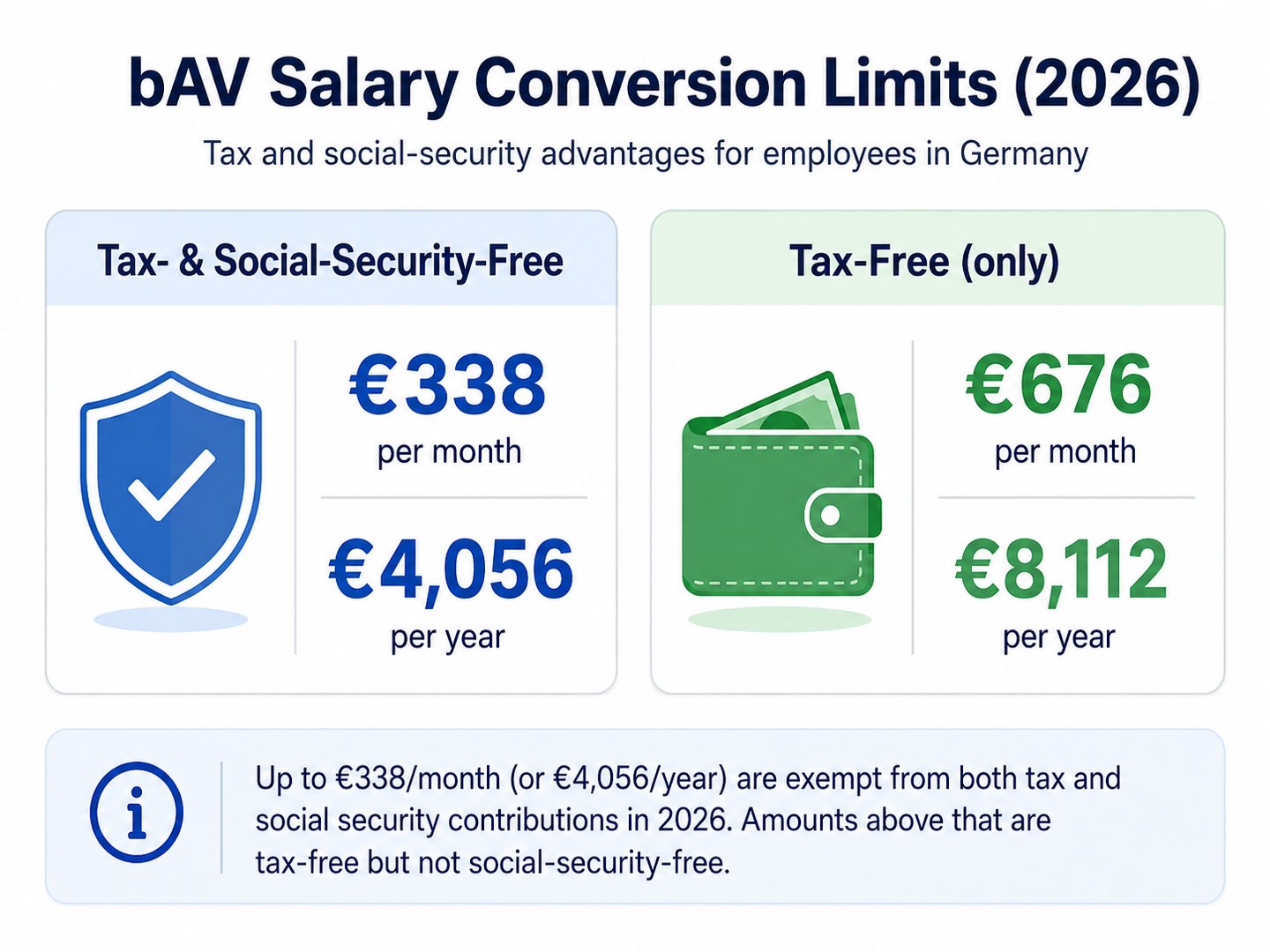

For 2026, employer contributions to occupational pension schemes are tax-free up to €8,112 per year. They are social-security-free up to €4,056 per year.

In monthly terms, this means:

For many employees, the first level — €338 per month — is especially attractive because it is both tax- and social-security-free.

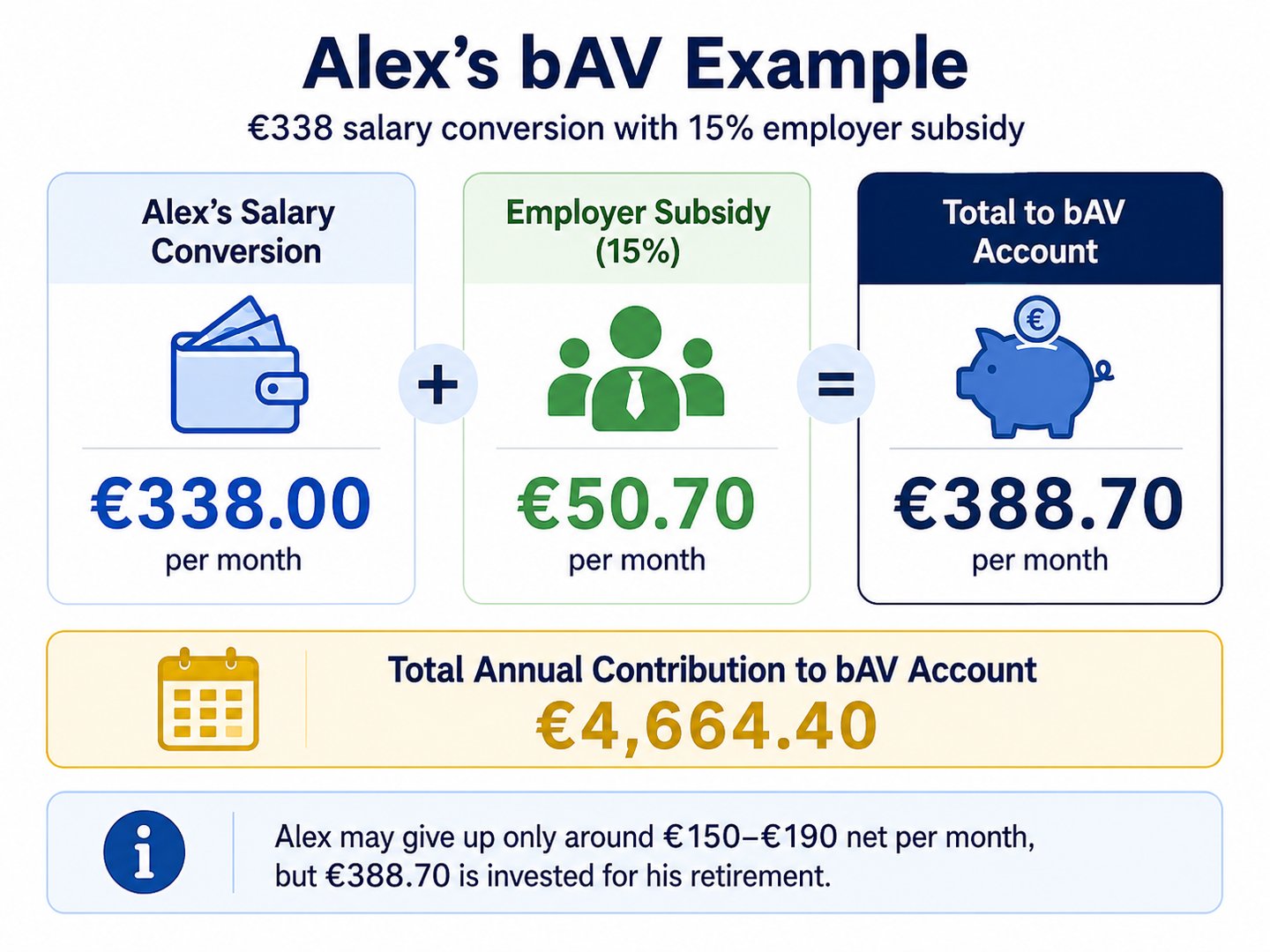

Alex’s bAV example: €338 salary conversion

Let us assume Alex decides to convert €338 per month of his gross salary into a company pension.

This is not the same as saving €338 from his net income.

Because the contribution is deducted from gross salary, Alex saves income tax and social security contributions immediately.

The effect could look like this:

The employer subsidy is important. Under § 1a of the German Occupational Pensions Act, the employer must generally pass on 15% of the converted salary as an employer subsidy to the pension fund, pension scheme, or direct insurance, to the extent that the employer saves social security contributions through the salary conversion.

In Alex’s example, this means:

Alex converts €338 per month, but €388.70 per month flows into his pension account.

Over one year, this creates €4,664.40 of retirement contributions.

The real net cost may be much lower

The psychological mistake many employees make is this:

They think that saving €338 means losing €338 of net income.

But with salary conversion, that is usually not the case.

Because the contribution is deducted from gross salary, Alex’s net salary might decrease by only around €150 to €190 per month, depending on his tax rate, health insurance, long-term care insurance, church tax, and personal situation.

At the same time, €388.70 per month is credited to his company pension.

That is the leverage of bAV:

Alex may give up roughly €170 net per month, but almost €389 per month is invested for his retirement.

This is why bAV can be one of the easiest entry points into tax-advantaged retirement planning for employees.

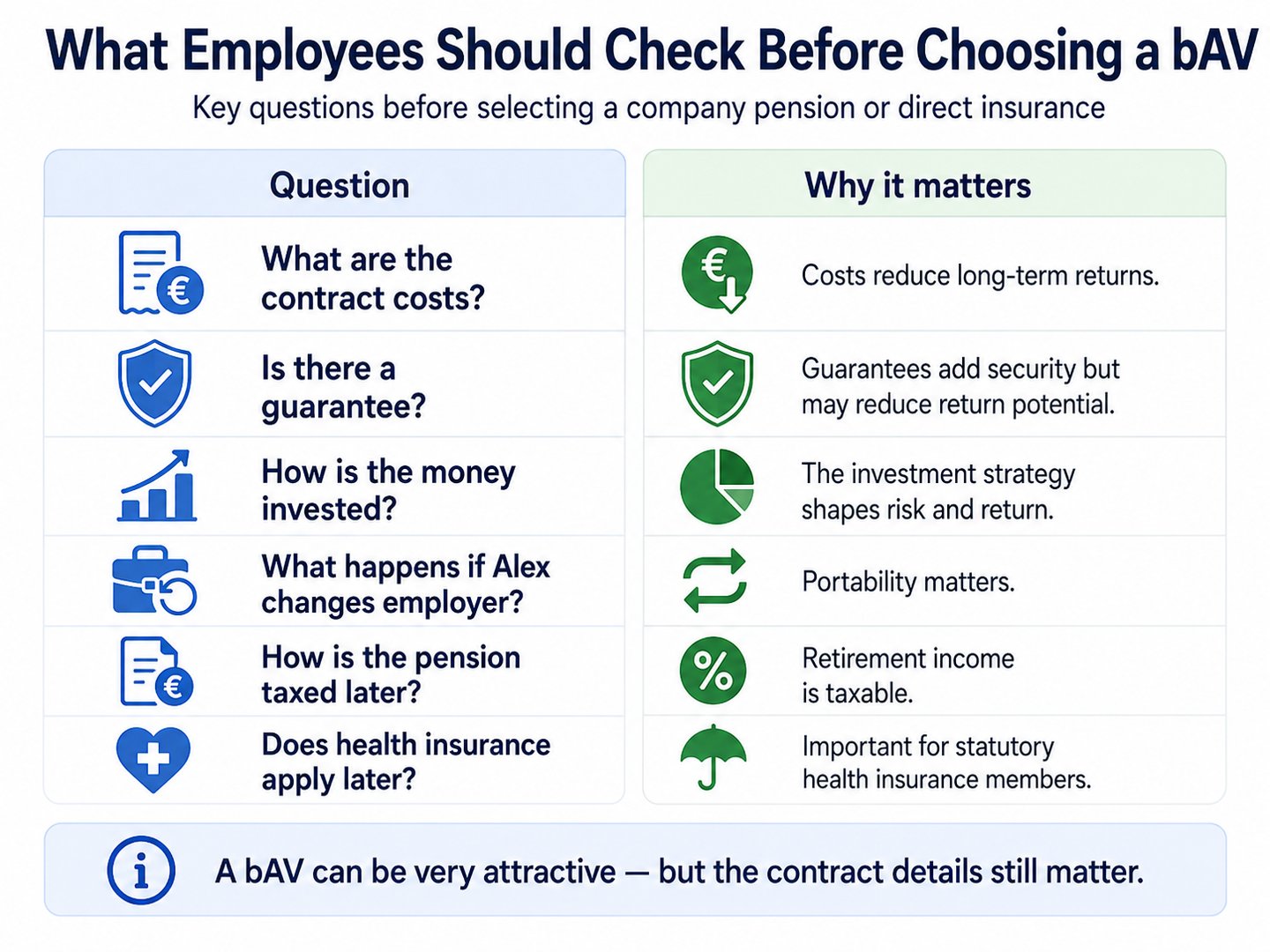

What happens to the money in the Direktversicherung?

A Direktversicherung is usually a pension insurance contract arranged through the employer.

The contributions can be invested depending on the product design.

Some products are more traditional and focus on guarantees. Others are more investment-oriented and may include funds, capital market participation, or ETF-related investment options.

For example, providers such as BarmeniaGothaer describe investment-linked direct insurance solutions that combine security, flexibility, and return opportunities, with participation in the capital market.

This does not mean that profits are guaranteed.

It means that Alex’s pension account may benefit from long-term capital market growth, depending on the selected tariff, guarantee level, costs, and investment concept.

A clean explanation for clients is:

The tax advantage and employer subsidy are relatively predictable. The investment return is not guaranteed.

Funds and ETF-based strategies can grow, but they can also fluctuate.

That is why Alex should review:

A bAV is attractive, but it should still be reviewed carefully.

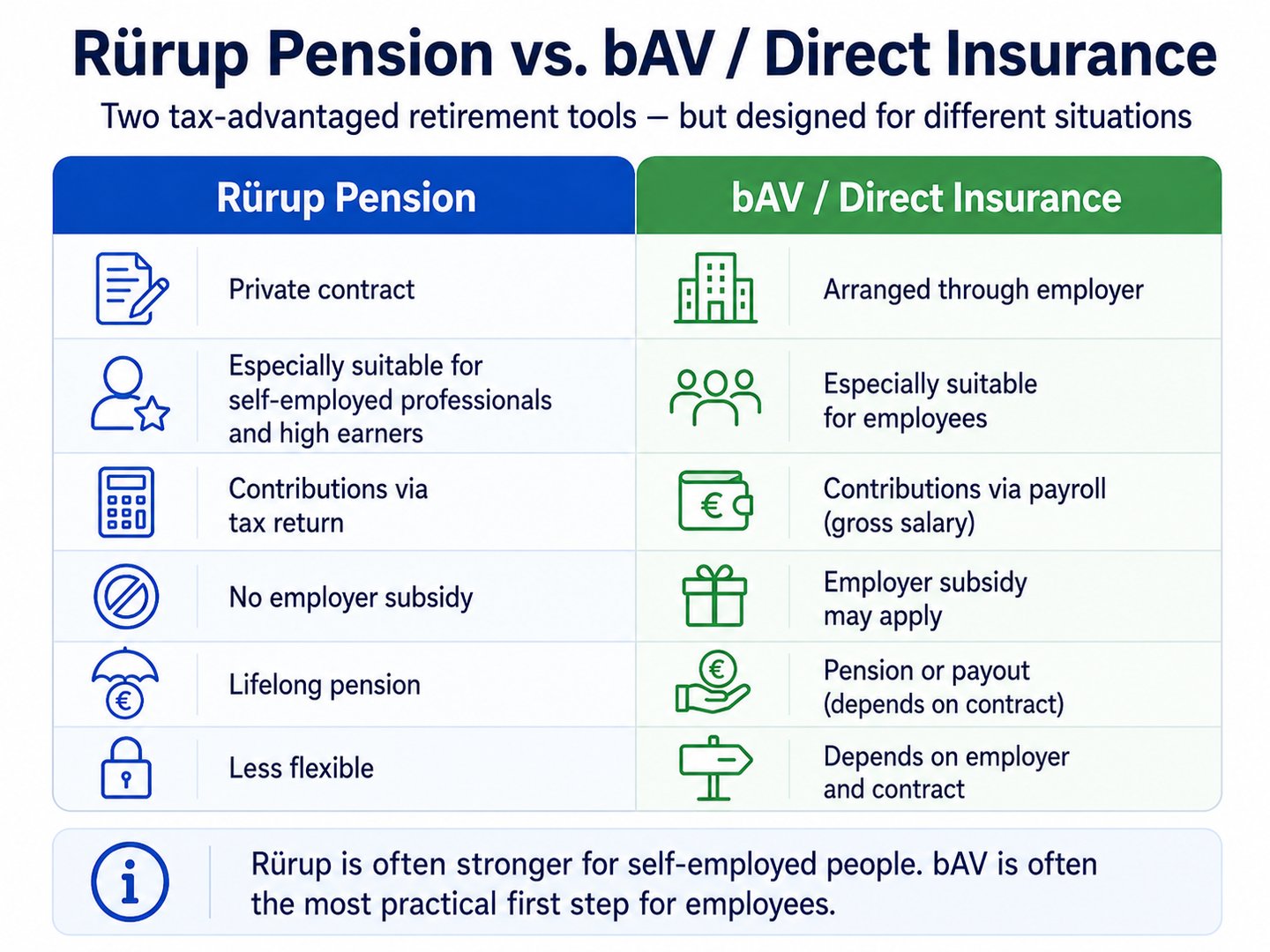

Why bAV is different from Rürup

Both Rürup and bAV are tax-advantaged retirement tools.

But they are not the same.

For Alex as an employee, bAV is often the more direct and practical first step.

He does not have to make a large annual contribution. He does not need to wait for the tax return to feel the effect. The process runs through payroll.

That makes the bAV very accessible.

Alex’s long-term effect

Let us keep the example simple.

Alex contributes through salary conversion:

€338 per month

His employer adds:

€50.70 per month

Total monthly contribution:

€388.70

Total annual contribution:

€4,664.40

If Alex continues this for 30 years without any increase, the total contributions alone would be:

€4,664.40 × 30 = €139,932

This is before possible investment returns.

If the money is invested over decades, the final value may be higher. But the result depends on markets, costs, guarantees, and product structure.

Still, the key message is strong:

Alex is not just saving a little tax. He is building a separate retirement account year after year.

Why this matters for foreign professionals in Germany

Many foreign professionals in Germany focus only on monthly net salary.

They ask:

“How much will I receive after tax?”

That is understandable. But it is only the first question.

The more important question is:

How much of my gross income can I convert into long-term assets?

Germany has a complex tax and social security system. But within that system, there are legal instruments to build retirement wealth.

For an employee like Alex, bAV can be one of the most practical instruments.

It allows him to:

use gross salary instead of net salary,

receive an employer subsidy,

build an additional retirement account,

possibly participate in capital market growth,

and reduce dependence on the statutory pension.

bAV is not a replacement for real estate or liquid savings

Alex may also want to buy a rental property later.

That can be a strong wealth-building strategy. But real estate usually requires equity, purchase costs, reserves, and financing capacity.

The bAV does not replace that.

Money inside a company pension is retirement money. It is not meant to be used freely for a property purchase.

Therefore, Alex should build several pillars:

The best strategy is not to put everything into one product.

The best strategy is to build a system.

Conclusion: Salary conversion turns income into retirement wealth

Alex earns a good salary.

But if he only consumes his salary every month, he remains dependent on the next payslip.

The bAV changes the structure.

With salary conversion, part of Alex’s gross income is transformed into retirement capital before it becomes taxable net income.

In the example, Alex converts €338 per month. With a 15% employer subsidy, €388.70 per month flows into his company pension. That is €4,664.40 per year in additional retirement contributions.

His net salary may decrease much less than the full contribution amount, because the payment comes from gross salary.

This is the core idea:

Alex does not become wealthy only because he earns €6,000 gross per month.

He builds wealth because he structures that income intelligently.

For employees in Germany, salary conversion and company pension schemes can be a practical first step from salary to long-term retirement wealth.

Important note: This article is a simplified educational example and does not replace individual tax, legal, or financial advice. Company pension rules depend on the employer, collective agreements, insurance provider, tax status, health insurance status, and the specific contract. Products with funds or ETF-related investments may fluctuate in value and do not guarantee profits.

Free Consultation

Have questions about entering the German market? Request a free consultation.

Request Free Consultation