Many international residents in Germany assume that once they are covered by statutory health insurance — the German gesetzliche Krankenversicherung, or GKV — most medical and dental costs are covered. For general medical treatment, that is often true. But dental care is one of the areas where statutory health insurance can leave patients with significant out-of-pocket costs.

This is especially relevant for people who plan to stay in Germany long term, including employees, students, freelancers, business owners, and families. While the German healthcare system is very strong overall, statutory coverage for dental treatment is limited when it comes to high-quality dental prosthetics such as crowns, bridges, inlays, dentures, and especially implants.

For this reason, many people in Germany take out a private dental supplementary insurance, known in German as Zahnzusatzversicherung.

Why Statutory Health Insurance Is Often Not Enough for Dental Care

German statutory health insurance generally covers basic dental treatment and contributes to medically necessary dental prosthetics. However, it usually does not cover the full cost of modern or premium dental solutions.

For example, if you need a crown, bridge, or denture, the statutory health insurance usually pays only a fixed contribution based on the standard treatment. If you choose higher-quality materials, ceramic solutions, aesthetic improvements, private dental treatment, or implants, you often have to pay a large part yourself.

Implants are particularly important. In most cases, statutory health insurance does not pay for the implant itself. It may only contribute to the prosthetic part placed on top of the implant, such as the crown. Additional procedures such as bone grafting can also become expensive.

Without dental supplementary insurance, the patient’s own contribution can quickly reach several thousand euros.

Why This Matters for International Residents in Germany

For international residents, dental insurance is especially important for three reasons.

First, many people stay in Germany longer than originally planned. A student may become an employee. An employee may start a business. A temporary stay may become permanent residence. Dental problems, however, often develop over time.

Second, many international residents are not fully familiar with the limits of German statutory health insurance. In many countries, dental treatment is either more private, more affordable, or structured differently. Germany has a very specific system: statutory insurance provides a basic framework, but premium dental care often requires private supplementary coverage.

Third, many foreigners maintain strong connections to their home countries. Some people may prefer to receive complex dental treatment — especially implants — in their country of origin because of language, trust, cost, or access to familiar dentists. This can be relevant for Korean, Japanese, Chinese, Vietnamese, Indian, Turkish, Arab, American, and other international communities living in Germany.

However, this is exactly where the details matter. A German dental supplementary insurance policy may cover treatment abroad, but the conditions must be checked carefully before treatment begins.

Two Strong Premium Dental Insurance Options in Germany

In this article, we compare two strong premium dental insurance options for people with statutory health insurance in Germany:

Barmenia Mehr Zahn 100

HanseMerkur Zahnzusatz Luxus EZL

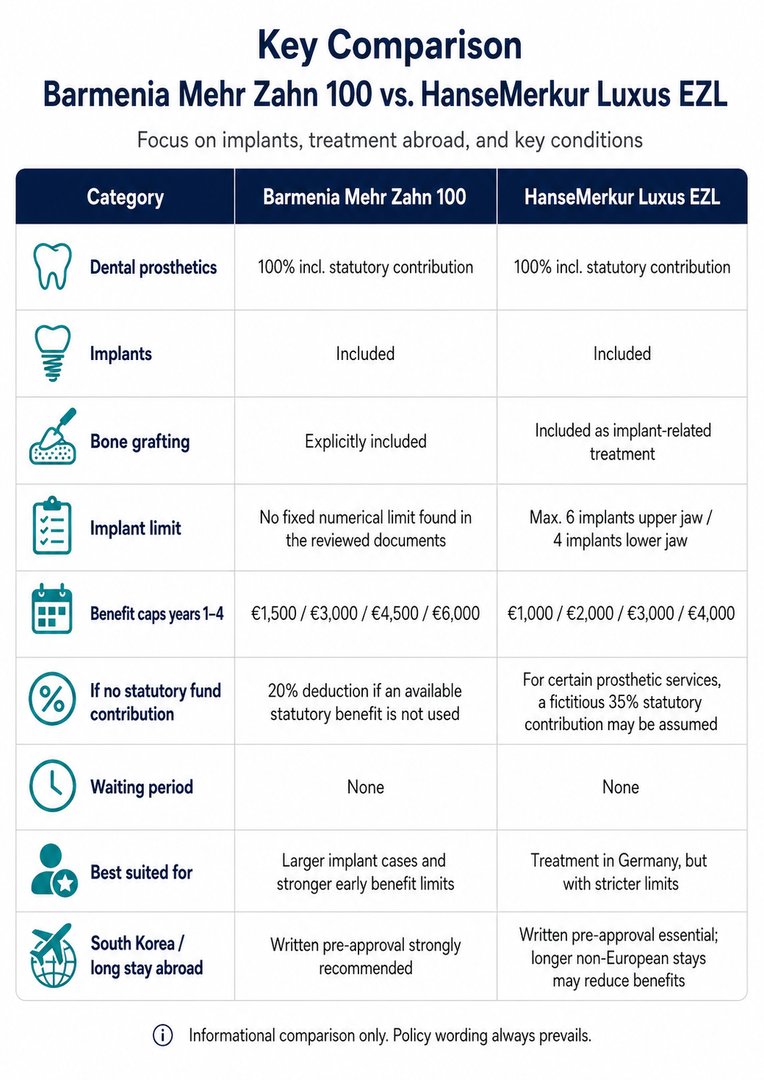

Both products are designed for people insured under the German statutory health insurance system. Both offer high reimbursement levels for dental prosthetics and implants. However, the differences become important when we look at benefit caps, implants, missing statutory insurance contributions, and treatment outside Germany.

1. Barmenia Mehr Zahn 100

Barmenia Mehr Zahn 100 is a dental supplementary insurance plan for people insured under German statutory health insurance or similar public healthcare systems.

The plan reimburses dental prosthetics such as implants, crowns, bridges, and inlays at 100% including the statutory health insurance contribution. It also includes related services such as pre-treatment, aftercare, functional analysis, functional therapy, and bone grafting.

This is especially important for people considering implants, because implant treatment often includes several cost components: the implant itself, the abutment, the crown, laboratory costs, imaging, and sometimes bone augmentation.

One important point: if a statutory health insurance benefit would normally be available but is not used, Barmenia may deduct 20% of the reimbursable invoice amount as a fictitious statutory contribution.

This can become relevant if treatment is carried out abroad and no German statutory health insurance contribution is obtained.

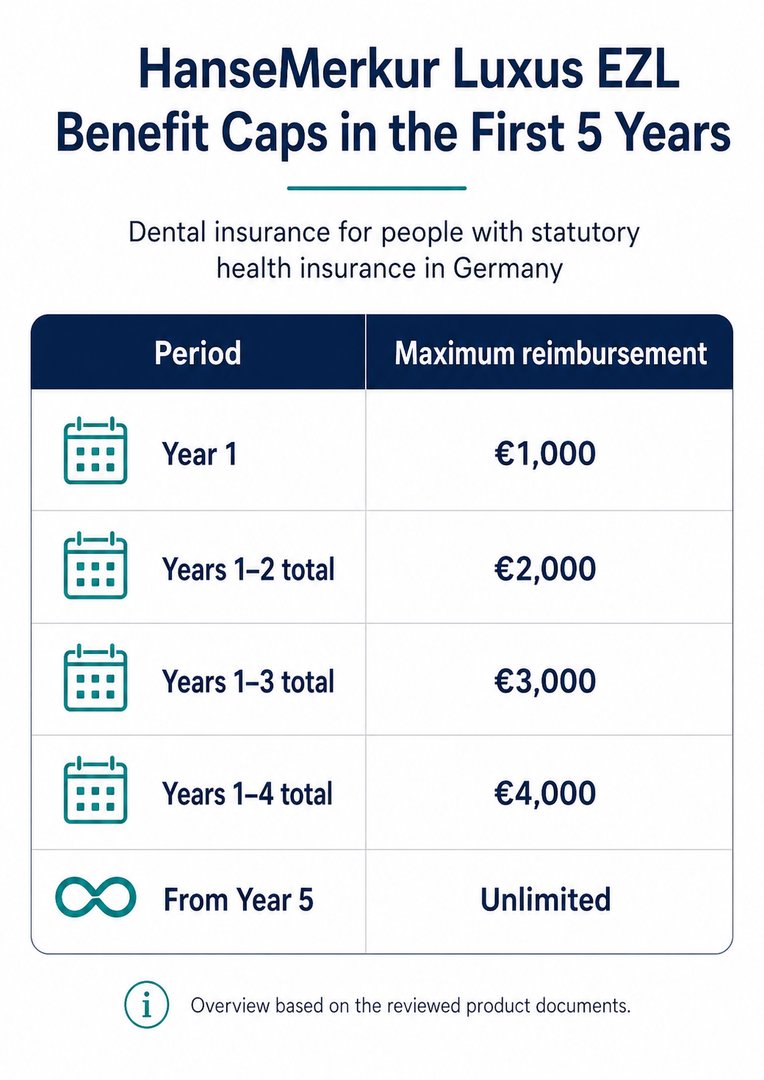

2. HanseMerkur Zahnzusatz Luxus EZL

HanseMerkur Zahnzusatz Luxus EZL is also a premium dental supplementary insurance plan for people insured under the German statutory health insurance system.

It offers 100% reimbursement for dental prosthetics including implants, again generally including the statutory health insurance contribution. It is a strong product for people who plan to receive treatment in Germany.

However, there are some points that international customers should pay attention to.

HanseMerkur mentions an implant limit of up to 6 implants in the upper jaw and up to 4 implants in the lower jaw. This may not matter for smaller implant cases, but it can be important for larger reconstructions.

The initial benefit caps are also lower than those of Barmenia Mehr Zahn 100.

Another important point: for certain prosthetic services, if no statutory health insurance contribution is documented, HanseMerkur may assume a fictitious statutory contribution of 35%. This can reduce the actual reimbursement, especially if treatment is performed abroad without prior coordination with the German statutory insurer.

What About Dental Treatment Abroad?

This is a key issue for international residents.

Many foreigners living in Germany consider dental treatment in their home country. This may be because they trust their dentist there, speak the language better, or expect lower costs. For example, Korean residents in Germany may consider having implants done in South Korea.

In principle, dental treatment abroad may be reimbursable, but this should never be assumed automatically.

Before starting treatment abroad, you should ask the insurer for written confirmation and submit:

a detailed treatment and cost plan,

a breakdown of implant, crown, abutment, bone grafting, laboratory, and imaging costs,

the expected treatment period,

confirmation whether German statutory health insurance will contribute,

confirmation whether a fictitious statutory contribution will be deducted,

confirmation whether the policy provides full coverage during the stay abroad.

This is especially important for treatment outside Europe. Longer stays outside Europe can be subject to special rules or reductions, depending on the insurer and policy wording.

Which Product Looks Better for International Residents?

Both products are strong premium dental insurance options. However, for international residents who may need larger implant treatment or who may consider treatment in their home country, Barmenia Mehr Zahn 100 appears more flexible and stronger in the early years.

The reasons are:

higher benefit caps in the first four years,

implants and bone grafting are clearly included,

no fixed implant number limit was found in the reviewed Barmenia documents,

the fictitious deduction without statutory contribution appears lower than in the HanseMerkur example.

HanseMerkur Luxus EZL remains a very strong option, especially for people who plan to receive dental treatment in Germany. However, the lower early benefit caps, implant number limit, and possible 35% fictitious statutory contribution should be checked carefully.

Conclusion

For international residents in Germany, dental supplementary insurance can be a very useful part of long-term financial and healthcare planning. German statutory health insurance provides a solid foundation, but it does not fully protect patients from high dental costs — especially for implants, crowns, bridges, inlays, and bone grafting.

For people who plan to stay in Germany long term, a good dental supplementary insurance can reduce financial risk and provide access to higher-quality dental care.

For international residents who may also consider treatment in their home country, such as South Korea or another non-European country, the key recommendation is simple:

Do not start treatment before receiving written confirmation from the insurer.

Based on the reviewed comparison, Barmenia Mehr Zahn 100 appears particularly attractive for larger implant cases and stronger early reimbursement limits, while HanseMerkur Luxus EZL is also a strong premium product but may be more restrictive in certain situations.

Final policy wording always prevails, and individual confirmation should be obtained before treatment.

********************************************

Link for Barmenia Mehr Zahn 100: https://ssl.barmenia.de/online-versichern/#/zahnversicherung/Beitrag?tarif=1&adm=01671312&fob=Zahnzusatz

Link for HanseMerkur Zahnzusatz Luxus EZL: https://secure2.hansemerkur.de/ola-ui2/1/100/tr/basisdaten?adnr=3211182&beragprtkhm=ja

Free Consultation

Have questions about entering the German market? Request a free consultation.

Request Free Consultation